Programmes

5 Mar 2026

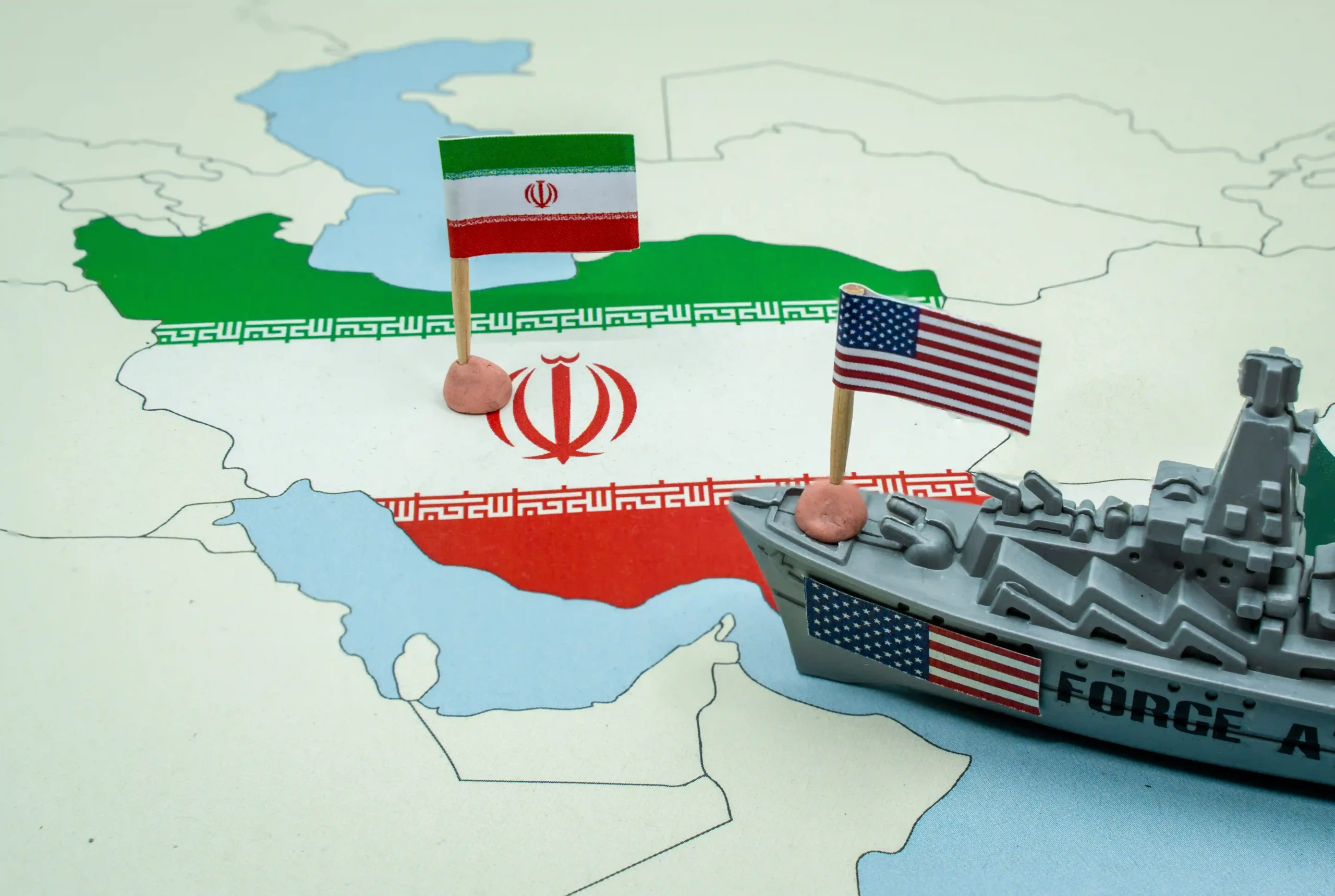

The Hormuz Inflection: Oil Markets After the Iran Strikes

The Feb. 28, 2026 United States–Israeli offensive against Iran represents the most consequential escalation in Gulf security dynamics in over a decade and introduces immediate, medium-term, and long-term risks to global energy stability. The strikes targeting senior leadership and strategic military infrastructure triggered Iranian retaliation across the Gulf region and sharply increased the probability of disruption to maritime energy flows, particularly through the Strait of Hormuz.

While physical supply outages remain limited at the time of writing, markets have responded by repricing geopolitical risk. Crude benchmarks surged on reopening, freight and insurance costs rose materially, and volatility spiked across commodities and currency markets. The core economic question is not whether prices react, they already have, but whether the conflict transitions from a risk-premium shock to a sustained supply disruption.

The Strait of Hormuz remains the central transmission channel. Roughly one-fifth of globally traded oil and more than one-third of seaborne liquefied natural gas pass through this chokepoint. Even temporary interference has outsized macroeconomic implications. Assessing the implications of the crisis requires examining immediate market reactions, potential disruption scenarios, medium-term supply responses, and the longer-term structural consequences for global energy security and macroeconomic stability.

Programmes

5 Mar 2026

The Missile and Drone Dilemma: When Defensive Measures Outstrip the Cost of Attack

The fundamental character of modern aerospace warfare has undergone an irreversible paradigm shift, transitioning abruptly from the deployment of exquisite, highly survivable platforms to the brutal arithmetic of industrial attrition and affordable mass. This operational reality was starkly illuminated in late February 2026, with the commencement of Operation Epic Fury by the United States Armed Forces and the parallel Operation Roaring Lion executed by the Israel Defence Forces.

Following the collapse of nuclear negotiations, the allied coalition launched a massive preemptive military campaign. Deploying an overwhelming concentration of aerospace assets, the coalition struck over one thousand strategic targets deep within Iranian territory during the opening twenty-four hours. United States forces executed over nine hundred individual precision strikes in the first twelve hours alone, utilising stealth bombers, naval fighters, and cruise missiles, escalating to more than one thousand, two hundred, and fifty targeted strikes within forty-eight hours. Simultaneously, the Israeli Air Force conducted over seven hundred sorties on the first day, dropping more than one thousand two hundred munitions to achieve immediate tactical successes and air superiority.

However, the immediate and sustained retaliation by the Islamic Revolutionary Guard Corps, designated Operation True Promise IV, has placed an unprecedented and mathematically gruelling strain on the allied integrated air and missile defence architecture. Within the first forty-eight hours of the conflict, the adversary entente launched roughly four hundred and twenty medium-range ballistic missiles targeting many countries in the region. This barrage was accompanied by massive swarms of loitering munitions.

The staggering depletion rates of multimillion-dollar interceptors and precision strike munitions against high-volume, low-cost adversary threats have exposed a profound mathematical vulnerability in contemporary military logistics. As the global defence industrial base proves incapable of replenishing these exquisite arsenals at the speed of combat consumption, both the allied coalition and the adversary entente are confronting a rapidly approaching logistical exhaustion horizon. To continue the war and secure a decisive strategic victory, it is an absolute strategic imperative for both sides to aggressively substitute these high-end, legacy assets with scalable, cost-asymmetric alternatives, pivoting their operational doctrines toward deployable mass and continuous attritional endurance.

Programmes

20 Feb 2026

China’s Tariff-Exemption Policy for Africa: Drivers and Outcomes

The Chinese Government, on Feb. 14, 2026, issued decisions abolishing 100% of customs duties on exports from 53 African countries. This step marks a significant shift in the trajectory of Beijing’s historic relationship with the African continent. This relationship began 70 years ago with major infrastructure ventures such as the construction of the Tazara Railway in the 1970s. It gradually evolved into an increasingly intricate framework of reciprocal economic integration.

This evolution has been reflected in the substantial expansion of bilateral trade, which reached a historic high of USD 348.1 billion in 2025, with annual growth of 17.7%. Through this new tariff-exemption framework, Beijing is voluntarily relinquishing approximately USD 1.4 billion in annual customs revenue upon the regime’s implementation, a move that constitutes a long-term geoeconomic investment aimed at reinforcing the stability of supply chains. This shift may reshape the global trade landscape and further position the African continent at the centre of intensifying competition for industrial resources and clean-energy technologies.

Accordingly, this analysis examines the strategic dimensions of this new trade regime by focusing on the updated structural dynamics of bilateral trade and their actual impact on Africa’s trade balance; the global competition to secure supply chains for critical minerals and the resulting implications for local industrialisation ambitions; and, finally, an assessment of the countervailing economic and political strategies adopted by Western blocs as they seek to reposition themselves and respond to expanding influence across the continent.

Programmes

10 Feb 2026

Digitising the Space Economy: Who Will Hold Sovereignty as the Shift from Hardware to Software Accelerates?

The global space economy is currently undergoing a profound structural transformation. Whereas the sector has historically been characterised by its heavy reliance on rocket propulsion capabilities and the vast capital investments required to deploy physical hardware into orbit, the focus is now shifting toward an economic model in which value creation is increasingly decoupled from material mass.

In this context, the contours of what may be described as a “software-defined space economy” are becoming increasingly evident. This shift is driven by the convergence of two core digital infrastructures: digital twins and space-based edge computing. At the same time, declining launch costs, resulting from advances in reusable launch vehicles, have shifted the primary determinant of economic efficiency. Rather than centring on mere access to space, value is now anchored in the operational efficiency of on-orbit assets, their embedded intelligence, and the length of their functional lifespan.

This paper argues that the sector’s future economic value—estimated to reach USD 1.8 trillion by 2035—will not be realised solely through an increase in the number of satellites launched, but rather through the digitisation of their life cycles and the processing of data at the source.

This analysis provides a comprehensive economic deconstruction of these technologies. It examines how “virtual modelling” is reshaping cost structures in space manufacturing, enabling companies such as Varda Space Industries and SpaceX to accelerate development cycles at software speed. It also highlights the roles of artificial intelligence and the Internet of Things (IoT) in establishing space systems capable of autonomous fault processing, thereby maximising returns by extending assets’ operational lifetimes. The analysis concludes by linking gains in operational efficiency to the sector’s overall growth, demonstrating how digital infrastructure forms the material foundation for emerging in-space manufacturing (ISM) markets and next-generation Earth observation services.

Programmes

7 Feb 2026

Transformations in the Uranium Enrichment Market and the Future of Global Energy

Since 2023, the uranium enrichment market has undergone its most profound structural transformation since the advent of the civilian nuclear era. After three decades characterised by persistent oversupply and the integration of Russian inventories with Western reactor fleets, the sector, valued at approximately $15.5 billion in 2025, now confronts a fundamentally altered geopolitical landscape. stems primarily from the fact that nearly 95% of global enrichment capacity is controlled by just four entities, placing Western supply chains under complex logistical and political pressures.

Central to this transformation is the evolution of what is known as the Separative Work Unit (SWU) from a readily available commodity into a strategic bottleneck capable of redrawing global energy maps. The market has shifted rapidly from a buyer-dominated structure to one characterised by seller leverage, amid an intensifying race to secure fuel for both conventional reactors and small modular reactors (SMRs), which require advanced uranium grades for which Western markets lack adequate commercial infrastructure.

Accordingly, this analysis explores the contours of the new enrichment landscape, examining the principal actors and evolving pricing dynamics, while projecting the profound implications of this transformation for global energy security.

Programmes

22 Jan 2026

The Implications of China’s Acquisition of a Lithography System

December 2025 marked a structural shift in the global technological balance of power, as a state-backed Chinese industrial consortium, coordinated by Huawei, approved the operation of a functional prototype of an extreme ultraviolet (EUV) lithography system at a facility in Shenzhen. This announcement dismantles a core assumption that has dominated geopolitical thinking in Washington, Brussels, and Tokyo over the past decade, namely that the extreme engineering complexity of EUV technology would permanently confine China behind a technological barrier, preventing it from advancing beyond the 7-nanometre threshold in leading-edge semiconductor manufacturing.

Western containment strategies were grounded in a firm conviction that the Dutch firm ASML’s monopoly over highly complex supply chains would guarantee the exclusion of the world’s second-largest economy from producing the advanced semiconductors required for artificial intelligence applications. The new Chinese prototype, however, has invalidated this assumption, not by replicating Western engineering paradigms, but by pursuing an alternative physical and engineering pathway, shaped by imperatives of national sovereignty and enabled by effectively unconstrained state capital.

This prototype, based on laser-driven plasma (LDP) technology, demonstrates that Chinese engineering teams have mastered the core physical principles of optical control at 13.5 nanometres. In doing so, they have moved beyond a phase long framed as one of "scientific impossibility", shifting the contest decisively into a new stage defined by engineering scale-up and operational viability. This development signals the end of an era of unipolar technological dominance. It inaugurates a new phase of dual ecosystems within the semiconductor industry. This transformation will require a comprehensive reassessment of the economic and security assumptions that have governed the sector for decades.

Programmes

2 Jan 2026

Gulf Sovereign Wealth Funds and the Video Game Economy

The structural foundations of the global video game economy are undergoing a profound transformation that extends well beyond the traditional triad of dominance in North America, Japan, and China. Strategic gravity is increasingly shifting toward the Gulf region, propelled by unprecedented capital inflows led by sovereign wealth funds across the Gulf Cooperation Council (GCC). This momentum marks a pivotal inflexion point in the investment doctrine of these institutions, most notably Saudi Arabia’s Public Investment Fund (PIF), alongside Abu Dhabi’s Mubadala and ADQ, and the Qatar Investment Authority (QIA). Collectively, they have moved beyond passive portfolio management focused on the accumulation of safe-haven assets such as US Treasury securities and real estate, toward active, operational ownership in high-growth technology sectors.

Within this context, the gaming industry, currently valued at over $200 billion and projected to surpass $300 billion by 2028, has emerged as a central pillar of this strategic shift. Its distinctive convergence with media ecosystems and artificial intelligence positions it as an ideal vehicle for advancing the economic diversification objectives embedded in national development visions.

Gulf engagement in this domain extends well beyond purely financial considerations into the realm of geopolitics. Through the acquisition of intellectual property, distribution networks, and digital infrastructure, these states are seeking to establish a form of “digital sovereignty” as an alternative to the historical dominance of hydrocarbons within their economic models. This objective is being pursued through differentiated strategies, ranging from Saudi Arabia’s vertically integrated approach to the United Arab Emirates’ ecosystem-building model and Qatar’s strategy of strategic linkage and connectivity.

Accordingly, understanding this investment domain requires situating it within the context of broader macroeconomic transformations. Successive price shocks in global oil markets, most notably in 2014 and during the 2020 pandemic and its aftermath, have exposed the limitations of the traditional petrodollar-based model in ensuring long-term wealth sustainability. By contrast, the gaming sector offers a structural response to pressing demographic challenges: it generates a jobs multiplier that exceeds that of many other sectors and absorbs the “youth bulge” that constitutes the overwhelming majority of the population, transforming it from a consumer base of foreign content into a national productive base that consolidates the principles of a new economic nationalism

Programmes

31 Dec 2025

The AI-Energy Crossroads: Can the World Build Enough Power to Sustain Intelligence?

In 2025, the rapid acceleration of artificial intelligence (AI) is no longer just expanding digital capabilities, it is reshaping the physical infrastructure that underpins the global economy. Data centres are becoming “AI factories,” designed for unprecedented computational intensity and continuous, large-scale workloads. Nearly 11,800 facilities were operating worldwide by 2024, with an increasing share built or retrofitted to power AI-grade computing. This shift has triggered a structural rise in energy consumption, placing extraordinary pressure on land, water, electricity systems, and financially straining grids and supply chains worldwide.

The defining constraint on the future of AI is no longer hardware or algorithms, it is energy. Without a rapid global shift to renewable and clean power, AI data centres will collide with resource shortages, grid instability, and economic risk, threatening the very growth they are meant to enable. As AI becomes foundational across industries, the challenge is no longer whether data centres will expand, but whether the world can generate enough clean power to sustain them. With demand already outpacing conventional grid capacity in major regions, energy availability not technological innovation will determine global competitiveness in the AI era.

Programmes

16 Dec 2025

Is AI a Catalyst for Economic Growth?

During the past decade, artificial intelligence (AI) has shifted from being an academic curiosity, becoming a driving force for reshaping economies worldwide. What once felt like speculative capabilities including machines generating code and automating complex workflows as well as optimizing global logistics and producing creative content, now became deployable tools on a larger scale across industries. AI’s rapid adoption raises several key questions among policymakers, economists and business leaders, most notably whether AI can contribute to the growth of national economic growth, and under what conditions do these gains materialize?

Macroeconomic models and strong empirical evidence suggest a positive outcome, however with notable limitations. AI, as a general-purpose technology, has more to offer than just efficiency improvements, it also functions as a key driver of innovation, productivity enhancement and transformation tool of economic structures. AI visibility and adoption have grown substantially, especially with the emergence of generative AI technologies such as exemplified ChatGPT, GitHub Copilot. This growth establishes AI as a valuable source of information and data, benefiting both firms and the border national economy, provided that this widespread adoption is backed and supported by a strong infrastructure and an adequate human capital, prepared to complement these technologies.

Programmes

25 Nov 2025

Beyond Rentals: Airbnb’s Bid to Dominate Hospitality

In 2025, Airbnb is no longer simply reshaping travel preferences, it is fundamentally altering the competitive landscape for hotels. What started as a short-term rentals (STR) platform has evolved into a diversified lodging ecosystem, offering private homes, boutique hotels, and curated local experiences through a single digital interface. This transformation has intensified pressure on traditional hotel operators, whose fixed costs, regulatory exposure, and legacy systems limit their ability to adapt. As travellers increasingly value flexibility, privacy, and authentic local stays, Airbnb’s asset-light model continues to draw market share away from lower- and mid-tier hotels particularly. AI-driven pricing, scalable supply, and global host networks enable the platform to respond to demand fluctuations faster than conventional accommodation chains.

As consumer preferences fragment and digital expectations rise, many hotels struggle to maintain occupancy, protect margins, and justify rate premiums. The crucial question is no longer whether Airbnb competes with hotels, but how profoundly its growth is reshaping hotel performance, strategy, and long-term sustainability. And with hotels now beginning to integrate into Airbnb’s platform, a deeper question emerges: in this evolving hybrid model, who ultimately stands to benefit more?

Programmes

7 Nov 2025

The 2025 American Economy: Navigating the Policy Crosscurrents of Tariffs and Tax Cuts

This analysis provides a comprehensive analysis of the United States economy as of November 2025, addressing the query of whether its current status is one of a "boom" or a "downslide." The principal finding is that the economy is exhibiting clear signs of downsliding in the immediate term. This assessment is substantiated by a pronounced deceleration in the labor market and a pre-emptive, counter-inflationary interest rate cut by the Federal Reserve, which has explicitly prioritized mounting employment risks over persistent inflation.

The 2025 economy is uniquely defined by the simultaneous implementation of two contradictory, multi-trillion-dollar policies. This has created a state of extreme tension and volatility:

A Contractionary Trade Shock: A new, aggressive tariff regime has been implemented, acting as a significant, broad-based tax on imported goods. This policy is demonstrably raising prices, eroding household purchasing power, and creating a drag on economic activity.

An Expansionary Fiscal Stimulus: The "One Big Beautiful Bill Act" (OBBBA) was passed, enacting a massive, deficit-financed stimulus by extending the 2017 tax cuts. This policy is designed to boost demand and investment.

The current "downsliding" dynamic is a direct result of the tariff shock's immediate contractionary impact, which has, for now, overpowered the stimulus. The Federal Reserve's October 2025 decision to cut interest rates confirms its judgment that "downside risks to employment" constitute the most immediate threat.

This analysisU.S. forecasts a volatile and unstable path. The 2025 slowdown is expected to give way to a temporary, stimulus-fueled "sugar high" in 2026, as the OBBBA tax cuts take full effect and boost demand. This artificial boom is projected to fade quickly by 2027-2028, revealing an economy structurally strained by a gross national debt exceeding $38 trillion, a persistent $1.8 trillion annual deficit, and a deteriorating net international investment position of -$26.14 trillion. The new policy mix has locked in this structural weakness.

Programmes

20 Oct 2025

The Ozempic Shockwave: How Is One Drug Impacting Global Food and Insurance Systems?

The worldwide rise of semaglutide—a marketed formulation under different names, most notably Ozempic—is occurring rapidly and in various ways. Since its initial approval for type 2 diabetes, Semaglutide has quickly adapted to drive changes in personal health behaviours, market dynamics, and healthcare policy priorities. The drug operates through a complex mechanism that alters the body’s appetite and metabolism, leading to the transformation. As a result, there is a widening divergence between its regulatory objective and a growing use as a weight loss tool.

The disconnect is not just clinical but a systemic coming together of prevalent cultural norms, insurance structures, pharmaceutical supply chains and global consumer trends. The increasing use of Semaglutide across different social classes and countries gives rise to important political economy challenges regarding the price of the therapy, access to it and the sustainability of national health systems.

This analysis examines semaglutide’s disruptive evolution from a drug invention to a global public health tool. The analysis focuses on the situation in the United States (U.S.), but it also examines future possibilities where affordability and scale could make the drug essential in combating obesity and metabolic disease.