The world economy is at a turning point, with a visible tendency to reverse the integration that was seen in the last decades of the 20th century. Growing scepticism about the benefits of globalisation, particularly in developed countries, accompanied the sluggish recovery after the Global Financial Crisis (GFC). This uncertainty led to a purposeful policy change away from integration known as geoeconomic fragmentation (GEF). A variety of policies impacting capital flows, worker mobility, and trade are included in GEF. GEF policies are motivated by a variety of factors, such as correcting internal economic inequities, economic competition, and national security concerns. Foreign direct investment (FDI), which has been declining recently, particularly in emerging countries, is another indication of how this trend toward GEF has affected FDI and the need for quick action to reverse it.

FDI Trends: Declining Flows and Emerging Risks

A significant fall in FDI has occurred recently, which can be attributed to the complex interaction between changing geopolitical conditions and global economic factors. Such a decrease has been particularly visible, with global FDI declining from 3.3% of GDP in the 2000s to 1.3% between 2018 and 2022. Moreover, net FDI into developing countries consistently declined, from an average of 3.7% of GDP in 2007 to 1.8% in 2019. This declining trend of net FDI persisted even after the COVID-19 pandemic, which limited profitable investments in developing countries.

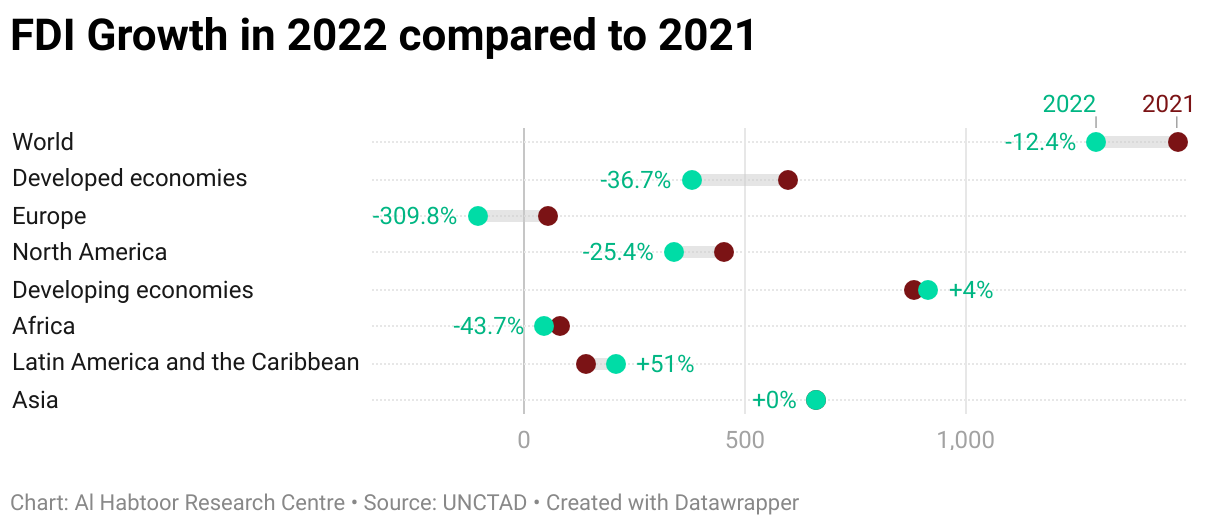

According to UNCTAD’s World Investment Report 2023, overlapping global crises caused FDI to fall 12% in 2022 to $1.3 trillion. Similarly, the latest Global Investment Trends Monitor from UNCTAD shows that while global FDI grew by 3% in 2023 to an estimated $1.37 trillion, the main driver of this overall uptick was a small number of European “conduit” economies, which frequently serve as intermediates for FDI intended for other countries. Unpredictably, global FDI flows in 2023 show a sharp 18% fall when these conduit economies are removed. The world’s largest recipient of FDI, the United States (U.S.), saw a 3% fall while the remainder of the European Union (EU) saw a sharp 23% decline. The research claims that worldwide FDI was sluggish, with reduced flows to emerging countries, where they dropped by 9% to $841 million, and dropping or stalling flows in most regions.

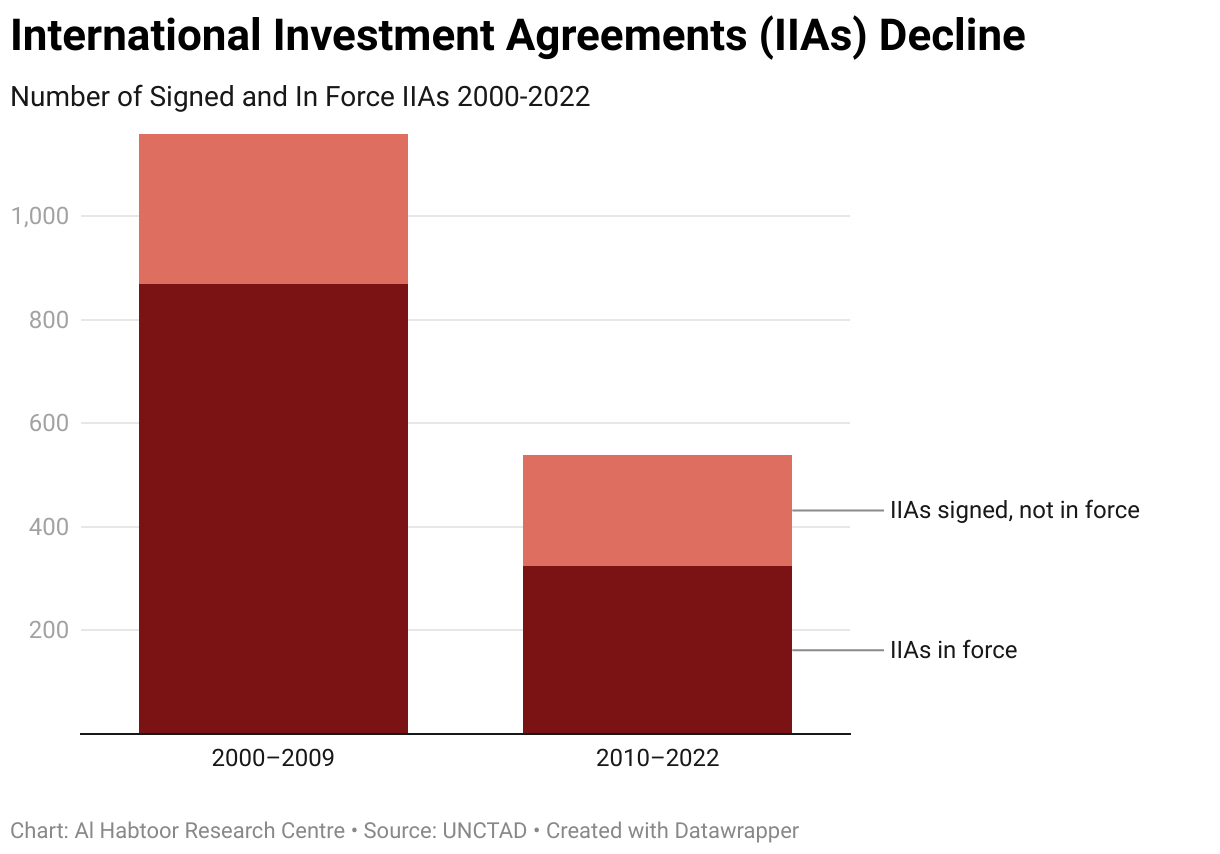

Moreover, FDI fell by 6% in China, 12% in Asia, 1% in Africa, and 47% in India, but remained stable in Latin America and the Caribbean, partly due to growth in Central America and the region’s second-biggest economy, Mexico, growing by 21%. In addition, the report highlights a concerning decrease in the number of foreign investment project announcements made in the previous year, particularly in the areas of project finance and mergers and acquisitions, which fell by 21% and 16%, respectively. Likewise, the number of international agreements declined from 1159 between 2000 and 2009 to 539 between 2010 and 2022. Among these agreements, 324 are currently in force, while 215 are signed but not yet in force.

As a result of the weak FDI performance in 2023, the UNCTAD expect a modest increase in FDI flows in 2024 but it warns that if significant risks persist, including mounting debt in many countries, and geopolitical tensions especially the onset of the Israel-Hamas War, might lead to further FDI decline due to security concerns and the preference for investors to invest in countries that are secure and politically aligned which constitutes the main driver of FDI fragmentation.

Drivers of FDI Fragmentation

A number of variables combine to cause FDI fragmentation, chief among them being the emergence of GEF, which describes the division of the globalised system into rival blocs motivated by ideological and political alignments. This trend is exemplified by the sluggish recovery from the GFC, geopolitical tensions like trade disputes between the U.S. and China, Brexit, and military conflicts. Tariffs, export restrictions, and other protectionist policies have been imposed as a result of U.S. trade competition.

The aforementioned actions have caused significant disruptions to long standing trade partnerships and supply chains, compelling companies to reevaluate their approaches to procurement and expand their production networks. Consequently, countries and regions are attempting to secure domestic sources of critical products and services and reduce their reliance on external suppliers; this is a trend toward regionalization. Consequently, in their investment decisions, governments and companies are placing a greater emphasis on security and resilience rather than purely economic efficacy.

Fragmentation has been further exacerbated by the COVID-19 pandemic and Russia-Ukraine War, which have also cast doubt on the advantages of globalisation and strained international relations. Although initially essential, the measures implemented in reaction to the pandemic have further complicated the situation and undermined confidence in open trade systems. Sanctions and heightened uncertainty regarding the trajectory of globalisation have resulted from Russia-Ukraine War, which has further strained international relations. Moreover, protectionism and cross-border restrictions have escalated due to geopolitical tensions, specifically in high-tech industries that are associated with national security. State-backed subsidy programmes and restrictions on FDI have increased the likelihood of global high-tech decoupling, which has negative repercussions for the global economy.

Indeed, the annual report on exchange arrangements and restrictions, published by the International Monetary Fund (IMF), sheds light on a significant increase in trade and capital flow limitations implemented by nations in 2020. These restrictions were notably imposed in response to national security concerns, according to the report. Significant recent developments encompass the U.S. Inflation Reduction Act, which contains provisions that incentivize domestic producers, occasionally to the detriment of their foreign counterparts. China, meanwhile, has launched the “Made in China 2025” initiative, a state-funded subsidy scheme designed to boost the country’s competitiveness in high-tech manufacturing. The EU has implemented the “Chips Act” to promote semiconductor technologies and applications within its borders. With regard to advanced computing and semiconductor manufacturing, the U.S. has recently implemented restrictions on the sale of particular high-tech products, software, and technologies to China.

Moreover, there is a growing emphasis among corporations on the resilience of their supply chains, as evidenced by the increased prevalence of corporate discourse surrounding reshoring, near-shoring, and onshoring. As a means of decreasing reliance on geopolitically precarious areas, reshoring pertains to businesses relocating production domestically. In contrast, friend-shoring pertains to the practice of corporations placing greater emphasis on investing in countries that are regarded as dependable allies. Although rational in nature, these approaches inadvertently result in the fragmentation of FDI inflows and less capital flows into emerging markets, which frequently lack geopolitical alignment with major economies, as investments become concentrated within blocs.

The 2023 IMF report “A Rocky Recovery” highlights a growing tendency for FDI inflows to be concentrated in countries that share similar geopolitical orientations. This alignment has a substantial influence on the geographical dispersion of FDI, particularly in relation to developing economies and emerging markets. This pattern has become more intensified since 2018, coinciding with the resurgence of trade disputes between the U.S. and China. Therefore, FDI is likely to concentrate within blocs of aligned countries in situations involving escalating geopolitical tensions and countries drifting further apart along geopolitical fault lines.

According to the IMF report, an analysis conducted using a multidimensional vulnerability index to FDI relocation, developing economies and emerging markets are, on average, more vulnerable to such relocations than developed economies. The primary source of this vulnerability arises from their dependence on FDI from countries with which they have limited geopolitical alignment. The fragmentation scenario remains a risk that is not limited to particular countries, as evidenced by the high susceptibility of numerous significant emerging markets in diverse regions to FDI relocation. The formation of blocs that impede the ability of developing countries to attract FDI, particularly those that are not aligned with the major economic powers, is occurring as countries place a greater emphasis on trading and investing with their allies.

Moreover, significant negative consequences are probable for host countries should FDI continue to decline and its geographical distribution alter. The aforementioned consequences would become evident in the form of decreased technological progress and capital accumulation, underscoring the criticality of fostering a climate that is favourable to FDI inflows and guaranteeing its fair allocation among countries. Additionally, the fragmentation of global production chains may result in inefficiencies, as organisations encounter difficulties in identifying dependable partners amidst geopolitical uncertainties. Investment reductions have the potential to limit employment generation, and impede economic expansion within developing countries. Studies conducted by the IMF indicate that a fragmented global investment landscape can result in significant output losses of approximately 2% of global GDP over the long term, with emerging economies bearing the brunt of these costs.

Cross-border finance and investment may experience a substantial decline if countries persist in diverging along geopolitical fault lines, according to a model developed by the IMF to compute the potential repercussions of geopolitical tensions. With a greater concentration of FDI within politically aligned blocs, corporate FDI is anticipated to decline further, resulting in a poorer global economy. Fragmentation also gives rise to substantial risk, such as escalated geopolitical tensions, increased inequality, and slower global economic growth. The IMF’s latest projections indicate that the expected annual growth rate of the global GDP in 2028 is a modest 3%, which is the most cautious five-year outlook in 30 years. As a result, poverty alleviation and the creation of employment opportunities, especially in developing countries with expanding youth populations, will face significant obstacles. This highlights the significance of sustaining a rules-based multilateral system and promoting global integration.

Mitigating FDI Fragmentation: Need for Action

It is necessary to promote global integration and adapt the multilateral system to address the challenges posed by escalating geopolitical tensions and fragmented FDI flows to mitigate FDI fragmentation. In response to the complexities of an increasingly fragmented global landscape, multilateral institutions must undergo transformation to prevent adverse repercussions on the global economy stemming from unilateral actions undertaken by dominant countries. The Investment Facilitation for Development (IFD) Initiative, which developing and least-developed World Trade Organisation (WTO) members launched in 2017, is a good example. Its objective is to establish a worldwide agreement that will improve the environment for business and investment. In Nov. 2023, following six years of rigorous work and open negotiations, the IFD Agreement was ultimately reached by all parties involved, and the agreement is now accessible for WTO members to join, having been published and finalised as of Feb. 2024.

In addition to capacity building and technical assistance, the IFD seeks to ensure that developing and least-developed countries receive special treatment. Furthermore, the IFD seeks to promote greater FDI inflows into developing countries amidst escalating protectionism and adverse effects on capital flows across borders. To support sustainable development, IFD is committed to fostering cross-border cooperation on FDI facilitation and improving the global investment climate. The agreement addresses matters such as sustainability, administrative practices, transparency of investment measures, while excluding market access and investor-state settlement to incentivize investments of higher quality.

The IFD has already the support of more than 120 WTO members, and its integration into the WTO regulations, which requires unanimous agreement, is necessary. The WTO can demonstrate its efficacy in addressing the concerns of its members amid global challenges by endorsing the IFD and assisting countries in attracting FDI and promoting sustainable development. In light of declining international investment flows and restricted FDI in developing and least-developed countries, research indicates that the elimination of investment barriers through IFD could result in substantial improvements in global welfare and prevent further FDI decline and fragmentation.

Ultimately, FDI fragmentation represents a concerning pattern that may have severe repercussions. In light of the dynamic geopolitical environment, it is imperative to acknowledge the perils associated with a fragmented international investment framework. Renewing the dedication to open and integrated markets and fostering multilateral cooperation are imperative to prevent FDI fragmentation and guarantee sustainable economic growth for all.

References

Ahn, JaeBin, Ashique Habib, Davide Malacrino, and Andrea F. Presbitero. “Fragmenting Foreign Direct Investment Hits Emerging Economies Hardest.” IMF, April 5, 2023. https://www.imf.org/en/Blogs/Articles/2023/04/05/fragmenting-foreign-direct-investment-hits-emerging-economies-hardest

Aiyar, Shekhar, Jiaqian Chen, Christian H Ebeke, Roberto Garcia-Saltos, Tryggvi Gudmundsson, Anna Ilyina, Alvar Kangur, et al. “Geoeconomic Fragmentation and the Future of Multilateralism.” IMF, January 15, 2023. https://www.imf.org/en/Publications/Staff-Discussion-Notes/Issues/2023/01/11/Geo-Economic-Fragmentation-and-the-Future-of-Multilateralism-527266

Commission, European. “Questions and Answers on WTO 13th Ministerial Conference.” European Commission , March 1, 2024. https://ec.europa.eu/commission/presscorner/detail/en/qanda_24_1288

Department of Economic and Social Affairs, United Nations. “World Economic Situation and Prospects 2024 |.” United Nations, January 4, 2024. https://www.un.org/development/desa/dpad/publication/world-economic-situation-and-prospects-2024/

Fund, International Monetary. “World Economic Outlook, April 2023: A Rocky Recovery.” IMF, April 11, 2023. https://www.imf.org/en/Publications/WEO/Issues/2023/04/11/world-economic-outlook-april-2023?cid=sm-com-tw-spring2023flagships-WEOEA2023001

Georgieva, Kristalina. “The Price of Fragmentation.” Foreign Affairs, October 19, 2023. https://www.foreignaffairs.com/world/price-fragmentation-global-economy-shock

Organization, World Trade. “Investment Facilitation for Development.” WTO, 2024. https://www.wto.org/english/tratop_e/invfac_public_e/invfac_e.htm

Sauvant, Karl P. “The WTO’s FDI Challenge.” Project Syndicate, February 22, 2024. https://www.project-syndicate.org/commentary/wto-must-approve-investment-facilitation-mechanism-by-karl-p-sauvant-2024-02?barrier=accesspaylog

Trade and Development, United Nations Conference on. “Global Foreign Direct Investment Grew 3% in 2023 as Recession Fears Eased.” UNCTAD, January 17, 2024. https://unctad.org/news/global-foreign-direct-investment-grew-3-2023-recession-fears-eased

Trade and Development, United Nations Conference on. “World Investment Report 2023.” UNCTAD, July 5, 2023. https://unctad.org/publication/world-investment-report-2023

Related Articles

The New Economics of Security: Priced for Permanence in a Fragmented World

Kharg Island: The Point of No Return

Iran’s Fragile Economic Adaptation Under Military Pressure

Is AI a Catalyst for Economic Growth?

Stock Market Decline: More Trouble for the Global Economy?

Comments