China, despite being the second-largest economy globally, encounters challenges such as a distressed real estate sector, reduced domestic consumption, and high debt levels. In response to these obstacles, the government is enacting policies aimed at encouraging domestic spending, mitigating the real estate downturn, and cultivating innovation to ensure sustainable development. The way these measures are implemented will not only impact the economic trajectory of China, but also that of the entire world.

Don’t Be Fooled

After the post-COVID reopening, China’s economy rebounded in 2023, with real GDP growth reaching the aim of about 5%. Domestic demand—especially private consumption—and fiscal spending, tax cuts, and looser monetary policy were the main drivers of this rebound. China’s economy got off to a solid start in 2024, with GDP growth beyond expectations as a result of the country’s successful manufacturing and services sectors. The first quarter of 2024 saw notable year-over-year gains in key economic indicators: retail sales increased by 4.7%, industrial added value by 4.5%, GDP by 5.3% to $4.1 trillion, and foreign trade increased by 5% despite a minor decrease in March. Industrial output and services continued to increase well in March despite a high base effect that caused growth to slow down. High-tech manufacturing and services, including business services and IT led the gains.

In addition, there was a 4.5% increase in fixed asset investment and a 6.2% increase in per capita disposable income. Due to robust supply and low domestic demand, the consumer price index remained flat and the unemployment rate was 5.2%. The manufacturing PMI increased to 50.8%, suggesting growth, with the manufacturing of high-tech and equipment exhibiting particularly strong development.

Despite these gains, the Chinese economy continues to face challenges, according to the most recent central bank survey, mainly related to the job market’s consumption expenditure, the country’s weak demand, and the decline in the real estate market. Through budgetary policies and job development initiatives, the government hopes to address these problems. It is especially focusing on the youth demographic, which has significant unemployment rates—in March, it was 15.3% for those aged 16 to 24 and 7.2% for those aged 25 to 29.

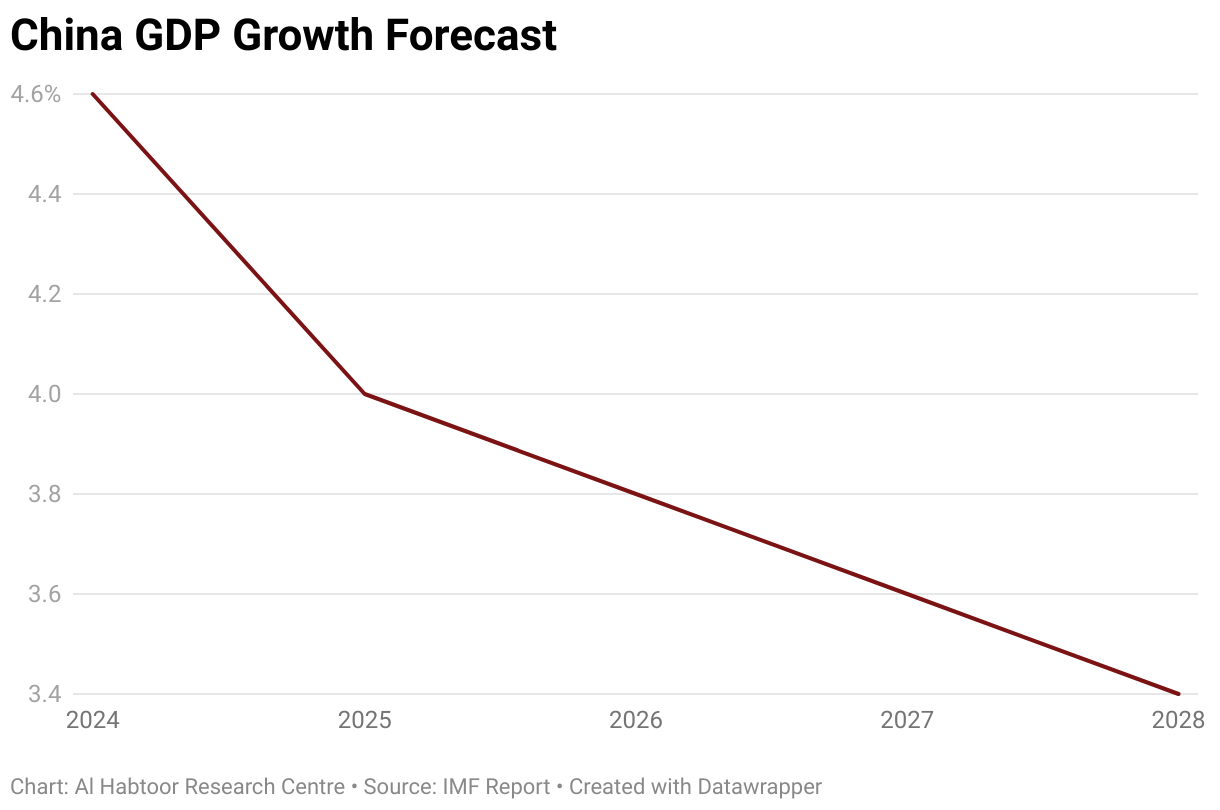

The central bank’s view is consistent with international institutions that view that China’s objective to achieve a 5% GDP growth in 2024 is very optimistic where the International Monetary Fund (IMF) predicts the growth to slow to 4.6% in 2024 before reaching 3.4% in 2028.

This downgrade can be attributed to the fact that China is facing challenges such as an ageing population, high debt, reduced domestic consumption, and a real estate crisis which is a major driver of the Chinese economy. For the past two years, China’s real estate market has been declining due to a protracted slump and a number of high-profile defaults, such as China Evergrande, which is burdened with more than $300 billion in debt. The root of the crisis can be attributed to regulations put in place in 2020 to prevent developers from taking on excessive debt, which caused a slowdown in sales and development. With an estimated 20 million pre-sold homes still unfinished, the industry needs significant funding to recover. With sales moving to the secondary market and the primary residential market predicted to contract significantly, the real estate market continues to be a major source of concern. The industry nevertheless has an impact on economic prospects even though some small cities have relaxed their purchase restrictions.

Expectations for an easing of monetary policy are heightened as China moves into the second quarter of the year and slowing economic growth is becoming apparent. Interestingly, the real GDP growth rate exceeded the nominal rate because of deflation, suggesting that growth would have been slower in the absence of deflation. The country’s gross fixed capital creation has been falling, which has an effect on overall investment, especially in the real estate industry. Economic development has been further squeezed by President Xi Jinping’s actions intended to burst the real estate bubble.

Additionally, state investment has also increased, although there are challenges due to growing public debt and constrained space for growth. The GDP contribution from net exports is not expected to reach past highs, and efforts to increase domestic demand are hampered by reduced household consumption spending and slowing growth rates. Economic indicators point to a softening in momentum, but worries about the real estate industry’s continued drag and the subdued demand from consumers and businesses prompted the government to step in with a number of initiatives to address those issues.

Government Response

To tackle the aforementioned challenges, the Chinese government is enacting several policies that are intended to boost internal demand and alleviate the decline in the real estate sector. In order to promote consumer confidence and stimulate spending, the government is implementing measures like subsidies, tax cuts and improvements to social welfare. More efforts are being made to increase accessibility to homeownership and stimulate housing market expenditure by loosening mortgage regulations and lowering down payment requirements. Instead of the previous minimum mortgage interest rates of 20% and 30%, the People’s Bank of China (PBOC) has eliminated the minimum mortgage interest rate nationwide and reduced the minimum down payment for first-time buyers to 25% and for second homes to 15%, respectively.

Furthermore, the government is encouraging local governments to acquire unsold homes and convert them into affordable accommodation in an effort to stabilise the real estate market. Potentially extending credit of up to $69 billion, the PBOC will provide $41.5 billion in loans to finance these state purchases. This helps alleviate urban housing shortages while also aiding developers in the clearance of their inventory. Policymakers are imparting a sense of urgency as official data released, a few days ago, showed that home prices in April recorded the largest monthly decline in a decade.

Real estate investment fell by 9.8% in the initial quarter of 2024 and new property sales fell by 28.3%, according to recent data. In order to further facilitate these acquisitions, substantial loan programmes are in place to support the financial assistance being extended to state-owned enterprises (SOEs).

In an effort to revive the government’s deteriorating real estate market, these measures are the most significant policies to date but they are still insufficient to solve excess inventory that will require an estimated of 1 trillion yuan. They are aiming to stabilize the market and revive investor confidence. However, the plan lacks detailed funding specifics since local governments, already heavily in debt, face challenges in executing these policies.

Furthermore, China intends to inject liquidity into the economy through the issuance of ultra-long bonds to finance key strategic projects as part of its efforts to stimulate growth. To bolster the economy, the government issued its first tranche of ultra-long special sovereign bonds, totalling $138 billion. The bonds, some of which were initially issued for 30 years, are intended to bolster infrastructure spending to face challenges such as a housing crisis and low consumer confidence. Monetary easing measures are anticipated to accompany the bond sales, which are expected to increase GDP by up to 1%, according to analysts.

Looking ahead, although these measures are significant and show the government seriousness to stabilize the market but they are only the initial steps that the government must undertake to maintain growth and it will take time. Regarding potential policy measures to stabilise the real estate market and bolster economic expansion, investors are awaiting indications from a significant government meeting that is scheduled for July.

Measures and Global Impact

According to the IMF report on China, the government should establish extensive structural reforms and encourage changes in the real estate industry in order to promote short-term economic activity, reduce risks, and guarantee a balanced transition to higher-quality growth. Restructuring unprofitable real estate companies, encouraging the construction of houses, and permitting market-based price adjustments are some of the main suggestions.

Fiscal strategies ought to concentrate on medium-term fiscal consolidation via social security and tax reforms, as well as lowering local government debt through financing vehicle restructuring. Enhancing risk-sharing between central and local governments and increasing household transfers will support recovery and strengthen the social safety net. Moreover, reforms in the financial sector should also focus on improving crisis management frameworks, identifying nonperforming assets, and strengthening prudential policies. Monetary policy transmission will be enhanced by loosening monetary policy and boosting exchange rate flexibility. By implementing pro-market policies, maintaining SOEs’ competitiveness, and enhancing labour market regulations—such as extending the retirement age—structural changes should increase productivity. Finally, trade and industrial difficulties can be addressed by reducing policies that have a negative spillover effect, minimising distorting industrial policies, accelerating SOEs reforms.

Consequently, China’s economic future will be greatly influenced by how well these policies will be implemented. Reviving domestic consumption could boost the economy’s other sectors and create a positive feedback loop that encourages additional expansion. By relieving the financial strain on developers and local governments, stabilizing the real estate market could lower the likelihood of a wider economic downturn. Meanwhile, maintaining long-term growth and making sure China maintains its competitiveness internationally depend on encouraging innovation.

These policies will have effects that go beyond China’s boundaries since China is a significant contributor to global trade, investment, and economic activity due to its status as the second largest economy in the world. China’s huge proportion of global output and quick expansion have had a profound impact on the dynamics of the global economy. It is the world’s biggest exporter and importer of goods, playing a key role in international supply chains and producing a vast range of goods. China has a crucial role in maintaining the stability and expansion of the global economy, as evidenced by its extensive influence as a major consumer market, manufacturing and technological leader, trade partner, and source and destination for investments. China was responsible for 18% of the world’s GDP, 15% of the world’s exports of products, and 30% of the world’s industrial value added in 2022.

A strong Chinese economy can boost demand for products and services from other countries, promoting international commerce and economic expansion. In contrast, extended economic challenges in China may result in decreased imports, a decline in the price of commodities globally, and volatility in the financial markets, which would affect economies around the world.

In conclusion, China’s ability to handle its current economic challenges will have a big impact on both the world economy and China’s own future. The policies being put into place are comprehensive and ambitious, seeking to solve pressing problems and establish the groundwork for long-term, steady growth. Policymakers, economists, and investors worldwide will be keenly monitoring these measures ‘efficacy because they have significant consequences for the stability and expansion of the global economy.

References

Cheng, Evelyn. “China’s Economy Reveals Pockets of Softness. Here’s What to Watch Ahead of Friday’s Data.” CNBC, May 14, 2024. https://www.cnbc.com/2024/05/15/chinas-economy-reveals-pockets-of-softness-ahead-of-fridays-data.html

Executive Board, IMF. “IMF Executive Board Concludes 2023 Article IV Consultation with the People’s Republic of China.” IMF, February 2, 2024. https://www.imf.org/en/News/Articles/2024/02/01/pr2433-china-imf-executive-board-concludes-2023-article-iv-consultation

He, Laura. “China Unveils ‘historic’ Rescue for Crisis-Hit Property Sector as Home Prices Slump Again | CNN Business.” CNN, May 17, 2024. https://edition.cnn.com/2024/05/17/economy/china-rescue-measures-housing-market-intl-hnk/index.html

Huld, Arendse. “China Q1 2024 GDP Expands 5.3%, Beating Growth Forecasts.” China Briefing News, April 17, 2024. https://www.china-briefing.com/news/china-q1-2024-gdp-grows-5-3

Kumar, Amit. “The Hidden Dangers in China’s GDP Numbers.” Foreign Policy, March 11, 2024. https://foreignpolicy.com/2024/03/11/china-economy-gdp-deflation-consumption/

News, Bloomberg. “China to Start $138 Billion Bond Sale on Friday to Boost Economy.” Bloomberg.com, May 13, 2024. https://www.bloomberg.com/news/articles/2024-05-13/china-to-hold-meeting-on-138-billion-ultra-long-debt-sale

Pao, J. (2024, May 17). China unveils property stimuli amid falling sales. Asia Times. https://asiatimes.com/2024/05/china-unveils-property-stimuli-amid-falling-sales/

Wakabayashi, Daisuke, and Claire Fu. “China’s Real Estate Crisis ‘Has Not Touched Bottom.’” The New York Times, January 30, 2024. https://www.nytimes.com/2024/01/30/business/china-evergrande-real-estate.html

Related Articles

Stock Market Decline: More Trouble for the Global Economy?

Saudi Arabia’s Economic Ascent and Persistent Challenges

Rise of Regional Investment Blocs: A New Era of FDI Fragmentation

Israel’s War is Testing its Economic Resilience

China’s Zero-Covid Policy: Impact on the Chinese Economy

What If the UN runs out of money?

What If: Iran Closed the Strait of Hormuz?

What If: China Invades Taiwan?

TikTok: China’s New Weapon

What If: The US Economy Collapses?

BRICS BRIDGE: Will Russia Reshape the Global Financial Order?

ASEAN’s Lessons: A Blueprint for Peace in the Middle East

Can the EU Endure Escalation in the Middle East?

Comments