The global economy has been struggling to recover since the impact of the COVID-19 pandemic, which has had significant repercussions worldwide. The European Union (EU) has been particularly affected by the Russia-Ukraine war due to its reliance on Russian energy. Following this conflict, the EU is gradually moving toward recovery, with an anticipated mild growth rate in 2024. However, the ongoing Middle East conflict and concerns about its potential escalation raise doubts about whether the EU can withstand the challenges posed by such an escalation.

2024: Charting Paths Through Global Challenges

The global economy has been significantly affected by the COVID-19 pandemic, leading to disruptions in supply chains and trade, increased inflation, and a global recession. Additionally, the Russia and Ukraine war has disrupted trade flows, driven up energy and food prices, and heightened uncertainty in financial markets. While an immediate escalation is not considered likely, the long-term geopolitical ramifications of the war could have significant economic consequences. The culmination of these events has fostered the anticipation that the global economy will undergo a recession in 2023 but unexpectedly, the global economy demonstrated resilience. Such resilience was buoyed by growth in emerging economies, a stronger labour market, China’s reopening, and resilient consumer spending.

Nevertheless, it is crucial to emphasize that steering clear of a recession should not be misinterpreted as an outright economic success. Challenges such as inflation, the potential for slowdowns in major economies, geo-economic fragmentation, and persistent geopolitical tensions continue to present risks. A clear example of geopolitical tensions is the Middle East conflict, which in case of its escalation, will have repercussions on the global economy that could surpass those of the Russia-Ukraine war. Navigating the complexities of 2024, the global economic landscape appears intricate and uncertain.

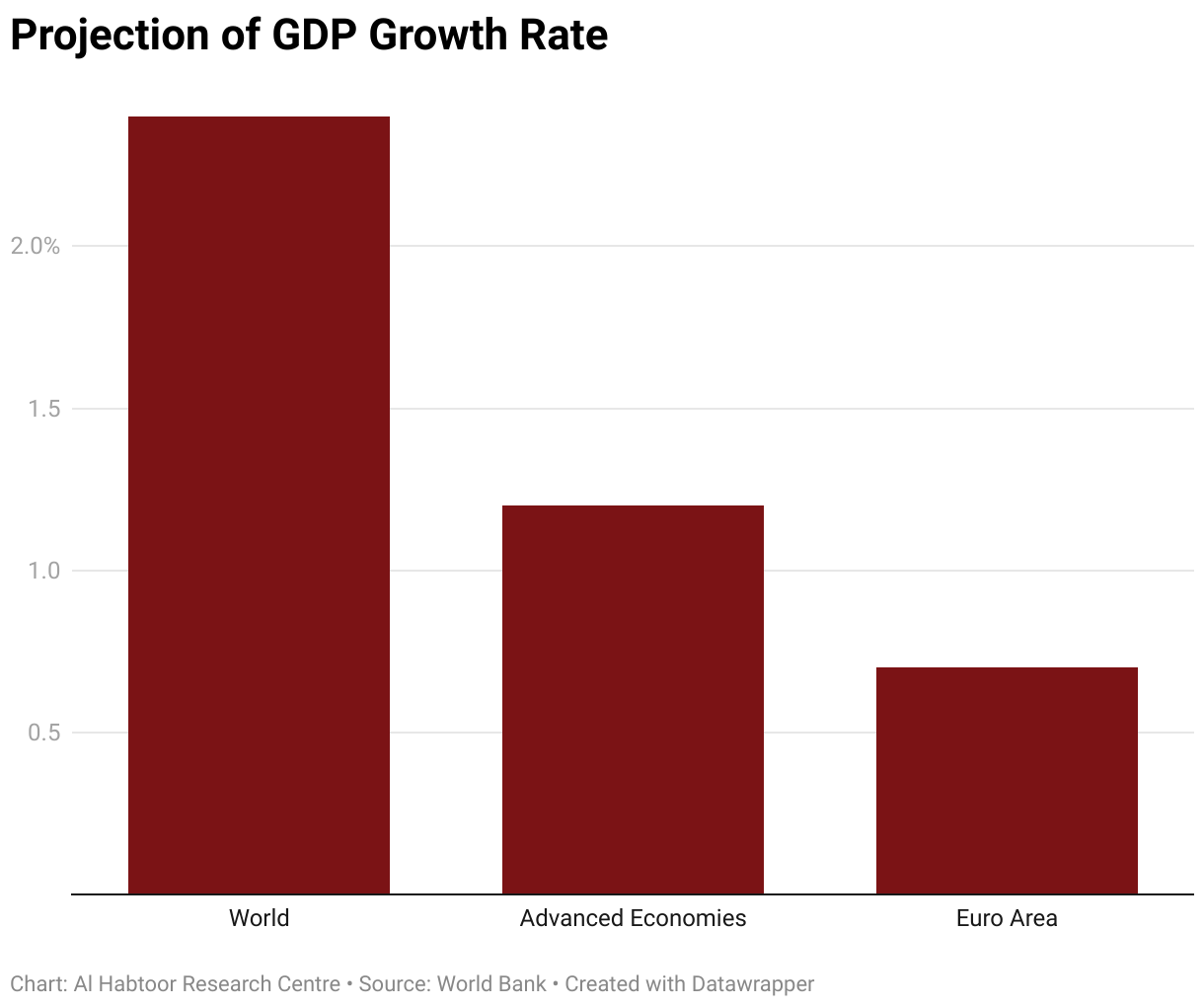

Currently traversing a challenging phase, global growth in 2024 is anticipated to be constrained due to stringent monetary policies and stricter credit measures. Several risks, including escalating conflicts in the Middle East, financial stress, a weakened Chinese economy, and climate-related disasters, loom as potential downsides. There is a possibility of experiencing a deceleration or even a mild recession in specific regions. The latest report from the World Bank, titled “Global Economic Prospects,” indicates that the global economy is on track for its weakest performance in half a decade. The forecast projects a third consecutive year of decelerating global economic growth, decreasing from 2.6% in 2023 to 2.4% in 2024. The growth outlook for developing economies is subdued at 3.9%, one percentage point below the previous decade’s average. Simultaneously, advanced economies are expected to witness a growth slowdown, dropping from 1.5% in 2023 to 1.2% in 2024.

Prospects for the EU’s Economic Future

Europe stands at a pivotal moment, following the severe energy price shock triggered by Russia’s invasion of Ukraine last year, the continent is now confronted with the challenging endeavour of reinstating price stability while concurrently fostering robust and environmentally sustainable growth in the medium term. Europe grapples with a demanding economic landscape marked by persistent inflation, elevated interest rates, a more stringent monetary policy, and escalating geopolitical tensions. The eurozone weakened in the second half of 2023, dragged down by tighter financing conditions, subdued confidence, and competitiveness losses. Growth slowed sharply in 2023 as the region continued to suffer the effects of the energy crisis and Germany, which accounted for 25% of the EU’s GDP in 2022, entered a recession, potentially exacerbating the challenges within the eurozone given its status as one of the strongest economies.

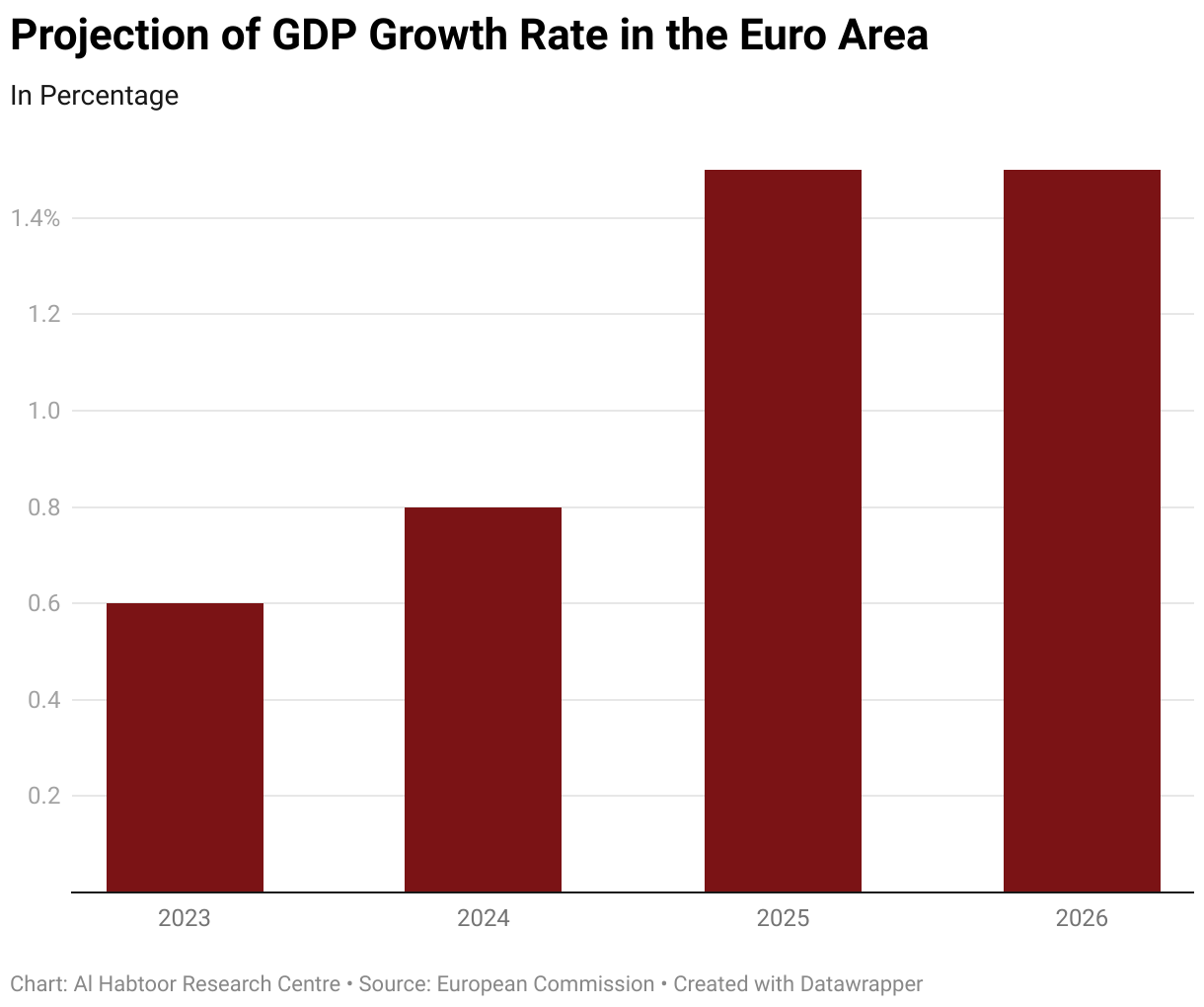

Nevertheless, there is an anticipation of strengthened growth from early 2024. This optimism is rooted in the rise of real disposable income, buttressed by decreasing inflation, robust wage growth, and the resilience of employment. Simultaneously, export growth is expected to align with improvements in foreign demand. The repercussions of the European Central Bank (ECB) tightening monetary policy and adverse credit supply conditions continue to influence the economy, impacting the short-term growth outlook. Forecasts indicate a gradual pickup in consumer spending, propelled by easing price pressures, real wage gains, and resilient labour markets. Additionally, there is a projection for a slow recovery in export demand following a subpar performance in 2023. Total investment growth in the EU is anticipated to accelerate to 1.5% in 2024, in contrast to 1.2% in 2023 and 2.3% in 2025. Overall, annual average real GDP growth is expected to recover to 0.8% in 2024 compared to 0.3% in 2023 and stabilising at 1.5% in 2025 and 2026.

Anticipated is a modest recovery propelled by an increase in consumer spending, facilitated by the alleviation of price pressures, the ascent of real wages, and the persistence of labour markets. However, the persisting and delayed impacts of tight financial conditions and the withdrawal of fiscal support measures are expected to partially counterbalance the positive effects of these growth drivers in 2024. Throughout 2023, the Federal Reserve and the ECB continued to raise interest rates, albeit at a more gradual pace, given that core inflation remained above the target.

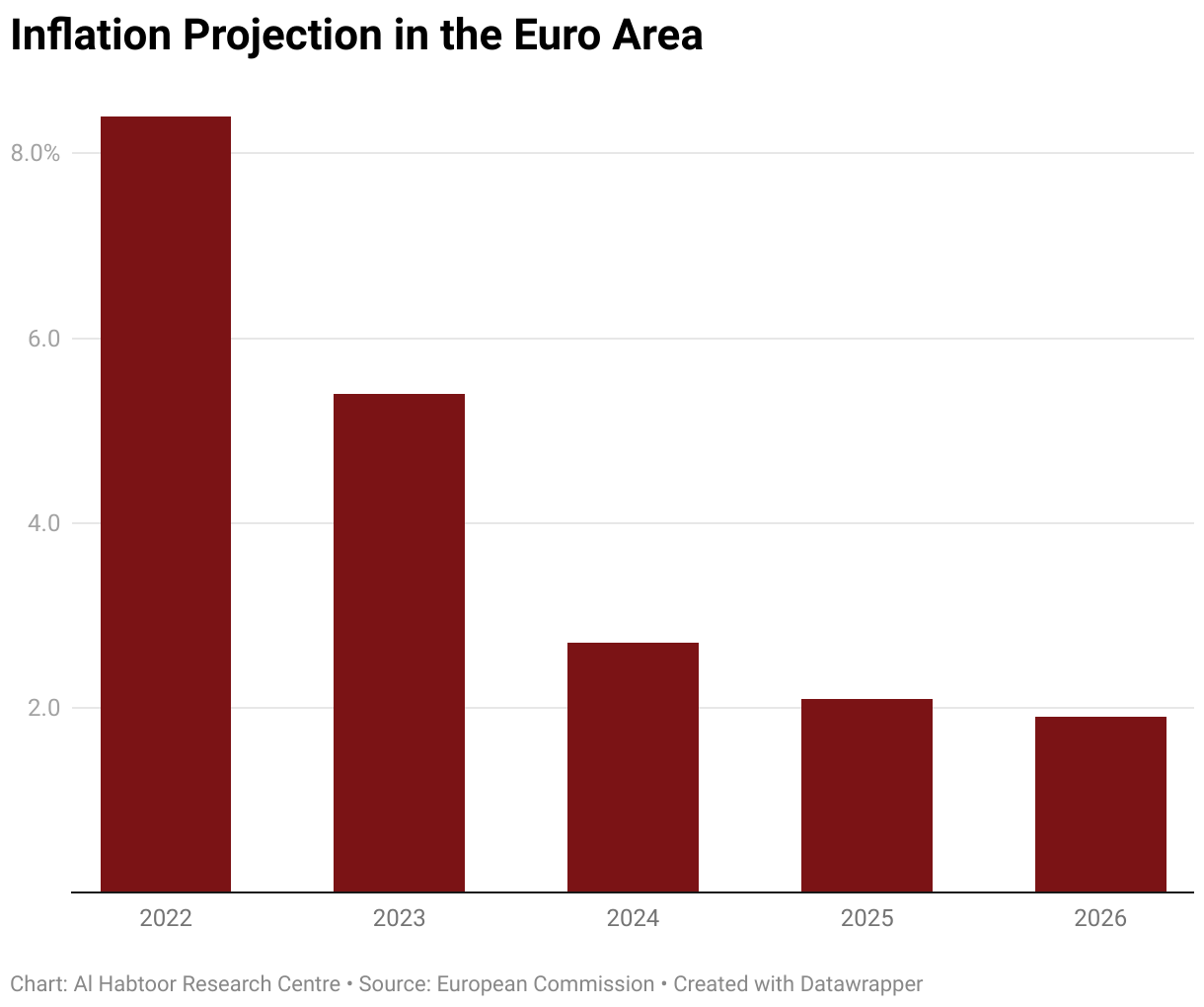

Central banks of major developed countries are poised to maintain higher interest rates for an extended period, driven by indications of increasing nominal wage growth, which signals the potential for second-round effects, and the possibility that escalating geopolitical tensions could reintroduce inflationary pressures. According to the IMF report on the regional outlook for Europe: “European emerging market economies will experience a mild recovery in 2024. Still, the extent will vary across countries depending on the energy intensity of production, service sector orientation, and, especially for the easternmost countries, disruption of trade relationships with Russia. Sustained nominal wage growth above inflation and productivity growth rates is a key risk to disinflation, especially in European emerging market economies. Inflation could become entrenched, requiring additional policy tightening and potentially leading to stagflation.”

Consequences of an Escalating Conflict

The recent Middle East conflict, layered upon Russia’s invasion of Ukraine, has significantly elevated geopolitical risks. The escalation of these conflicts or a rise in geopolitical tensions in other regions could adversely impact the global landscape through commodity and financial markets, trade disruptions, and a decrease in confidence, subsequently affecting investment and potentially causing a further decline in growth. An escalated conflict in the Middle East would resonate throughout the global economy, causing shockwaves that would extend to the borders of the EU. Disruptions to the supply of oil and gas, vital imports for the bloc, could potentially lead to a surge in energy prices. This escalation may contribute to inflation and has the potential to initiate a recession. Such a scenario would disrupt crucial industries and impose difficulties on consumers, particularly those in energy-intensive sectors such as transportation and manufacturing.

Indeed, the ongoing assaults on commercial vessels navigating the Red Sea for an extended period, affecting a vital waterway constituting 12% of global trade traffic, raise concerns. The escalating tensions may influence the trajectory of inflation as energy prices fluctuate. These attacks have begun to interfere with crucial shipping routes, diminishing slack in supply networks and heightening the potential for inflationary bottlenecks. Equally noticeable is the impact of the attacks on shipping in the Suez Canal where it saw a daily movement of only 200,000 standard containers, a significant decrease from approximately 500,000 containers in November 2023, as reported by the German think-tank Kiel Institute. Additionally, the drone attack targeting the U.S. base on the Jordan-Syria border led to a marginal increase in crude oil prices by 0.27%, reaching $78.2 on Jan. 28, marking a weekly rise of 4.73%, and Brent crude oil prices witnessed a 0.05% uptick to $82.9, with a weekly gain of 3.70%.

The Suez Canal, along with the Arab Petroleum Pipelines Company (SUMED) pipeline and the Bab al-Mandeb, serves as crucial pathways for Gulf oil and natural gas shipments destined for Europe and North America. According to the U.S. Energy Information Administration, in the first half of 2023, these routes facilitated around 12% of the total seaborne-traded oil, while also contributing to approximately 8% of the global liquefied natural gas (LNG) trade. The partial or complete closure of any of these straits poses a direct risk to the oil supply for Europe.

Furthermore, in the event of an escalation leading to the war expanding into a regional conflict with Iran actively participating, the U.S. is expected to intensify the enforcement of international sanctions on Iran’s oil exports. This, in turn, could prompt Iran to retaliate by engaging in harassment or attempting to obstruct the shipping of oil and LNG cargoes through the Strait of Hormuz. Notably, the Strait of Hormuz stands as the world’s most critical oil chokepoint, with an average oil flow of 21 million barrels per day in 2022, equivalent to approximately 21% of global petroleum liquids consumption. The ongoing geopolitical instability and tensions between Iran and the U.S. are poised to further elevate oil prices, fuelled by the escalating uncertainty in the Middle East, subsequently contributing to an increase in inflation. This presents an additional challenge for Europe, which is already grappling with gas import concerns due to the conflict in Ukraine and prevailing high prices. The potential partial or complete closure of the Hormuz Strait would bring disruptions in economic activity, leading to elevated energy and commodity prices, as well as an upswing in broader economic uncertainty and disruptions in financial markets.

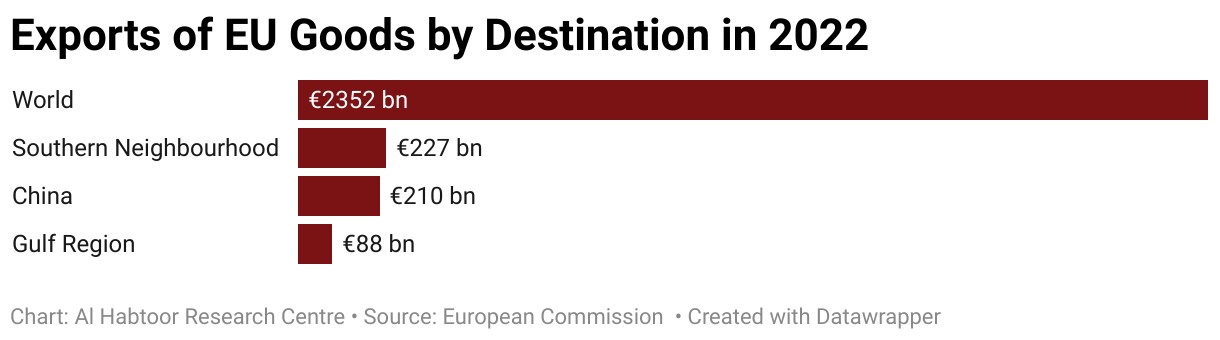

Additionally, with regards to trade, the extra-EU exports of goods totalled 2352.1 billion euros globally as of November 2022. These included exports amounting to 227.2 billion euros to the Southern Neighbourhood countries (Algeria, Egypt, Israel, Jordan, Lebanon, Libya, Morocco, Palestine, Syria, Tunisia), €210 billion to China, and 87.8 billion euros to the Gulf Region. In the case of international spillovers, it could negatively impact foreign demand for EU exports, leading to a further decline in aggregate demand.

Additionally, as per Eurostat statistics from 2022, the trade between Europe and Asia holds considerable importance where the EU recorded substantial imports amounting to 626 billion euros from China, accompanied by exports totalling 230 billion euros. Disrupting this trade flow could lead to significant financial losses, running into billions of dollars, directly affecting the EU economy.

Moreover, the tourism sector, a crucial revenue source for numerous EU member states, would face adverse effects. Potential security issues and travel disruptions would discourage tourists from visiting countries near the conflict zone, negatively impacting economies heavily dependent on hospitality and leisure.

Therefore, should the situation escalate, it is anticipated that inflation will increase within the eurozone, accompanied by elevated energy prices and a decrease in trade, investment, and tourism. Projected outcomes include reduced economic growth in both 2024 and 2025, ultimately resulting in a contraction of GDP.

References

Bank, World. “Subdued Growth, Multiple Challenges.” Global Economic Prospects. Accessed February 3, 2024. https://www.worldbank.org/en/publication/global-economic-prospects.

Commission, European. “EU Trade Relations with Gulf Region.” Trade. Accessed February 1, 2024. https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/gulf-region_en.

Commission, European. “EU Trade Relations with Southern Neighbourhood.” Trade. Accessed February 1, 2024. https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/countries-and-regions/southern-neighbourhood_en.

EIA. “The Strait of Hormuz Is the World’s Most Important Oil Transit Chokepoint – U.S. Energy Information Administration (EIA).” The Strait of Hormuz is the world’s most important oil transit chokepoint – U.S. Energy Information Administration (EIA). Accessed February 2, 2024. https://www.eia.gov/todayinenergy/detail.php?id=61002.

EIU. Energy outlook 2024 – eiu.com. Accessed February 4, 2024. https://www.eiu.com/n/wp-content/uploads/2023/10/Energy-report-2023.pdf.

Gentiloni, Paolo. “Autumn 2023 Economic Forecast: A Modest Recovery Ahead after a Challenging Year.” Economy and Finance. Accessed February 4, 2024. https://economy-finance.ec.europa.eu/economic-forecast-and-surveys/economic-forecasts/autumn-2023-economic-forecast-modest-recovery-ahead-after-challenging-year_en.

Hinz, Julian, and Mathias Rauck. “Kiel Trade Indicator 12/23: Cargo Volume in the Red Sea Collapses.” Kiel Institute. Accessed February 4, 2024. https://www.ifw-kiel.de/publications/news/cargo-volume-in-the-red-sea-collapses/.

IMF. “Restoring Price Stability and Securing Strong and Green Growth.” IMF, November 8, 2023. https://www.imf.org/en/Publications/REO/EU/Issues/2023/10/13/regional-economic-outlook-for-europe-october-2023?cid=ca-com-compd-pubs_rotator-AM2023.

Perkins, Robert. “Maersk Suspends Container Voyages through Bab Al-Mandab Strait Due to Attacks.” S&P Global Commodity Insights, December 15, 2023. https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/oil/121523-maersk-suspends-container-voyages-through-bab-al-mandab-strait-due-to-attacks.

Ruffino, Greta. “EU Price Rises on the Cards? Expert Insight on Red Sea Economic Impact.” Euronews. Accessed February 1, 2024. https://www.euronews.com/business/2024/01/31/expert-insights-how-is-the-red-sea-crisis-impacting-the-economy.

Related Articles

The Fallout of Escalating Iranian-Israeli Tensions

The Consequences of Social Media and Memes as a Theatre of War

War, Pressure and Policy: Europe’s Gradual Turn on Israel

From Doha to Washington: How Hormuz Redrew Global Gas Supply Chains

The Implications of the April 2026 U.S.–Iran Ceasefire on Oil Prices

Comments