Programmes

15 May 2026

US-China Summit: Not Peace, Rivalry Management

In the early hours of May 13, US President Donald Trump travelled to China to engage in high stakes talks with his Chinese counterpart Chinese President Xi Jinping. These talks are taking place in the context of heightened global instability stemming from conflicts such as the US-Israel-Iran War and the economics shocks stemming from this conflict. Within this context, both governments are set to engage in conversations aimed at stabilizing the US-China relationship and partaking in strategic dialogue regarding geopolitical and economic uncertainty. This summit can potentially shape the future of the US-China relationship as the outcome of these talks can shape the economic and security relationship between the two nations and their partners in the long run. Therefore, an exploration into this summit is needed and will focus on explaining the reason the summit is happening now, the mindset of the parties entering the summit, the topics on the agenda, and the potential outcomes of the summit.

Programmes

25 Mar 2026

Iran as a Potential Arena for Great Power Competition

The U.S.-Israel-Iran War is well underway, and the risks of spillover and enlargement is becoming more of a reality as the war goes on. As the conflict continues to expand, several actors are seeking out opportunities to challenge the existing balance of power in the region and aim to exploit the war to expand their influence. In the past decade, Russia has been working to court the United States’ MENA allies into its sphere of influence through the concept of regime stability, while China is taking on a soft power approach through economic and diplomatic cooperation. A prolonged war between the U.S.-Israel and Iran can result in global powers such as Russia and China getting more involved in the region to diminish American influence globally, which can result in a great power competition. The potential of Iran serving as an arena for great power competition will be explored through the American strategic overstretch and the economic shock caused by energy crisis.

Programmes

22 Mar 2026

From Partnership to Prudence: China’s Changing Investment Posture in Israel

Economic and geopolitical relations between China and Israel have undergone significant changes following the War on Gaza. Chinese regulatory authorities moved to classify certain areas within Israel under what is known as the Red Category, an official administrative designation that identifies these locations as high-risk investment zones. This classification imposes legal restrictions that prevent the injection of new financial investments into these areas.

As a result, a legal environment has emerged in which Chinese companies rely on security warning protocols and personnel safety considerations as a formal justification for controlling capital flows and suspending the implementation of certain financial obligations under previously signed contracts. This development necessitates a careful examination to understand how these risk assessment mechanisms operate and their tangible impact on the economic relationship between the two countries.

Programmes

19 Mar 2026

Strait of Hormuz Closure: Strategic Implications for the Global Semiconductor Industry

Iran has blocked maritime navigation through the Strait of Hormuz since the first week of March, following the attacks it sustained during Operation Epic Fury. This disruption has hindered the movement of nearly 20 million barrels of crude oil per day. It has trapped shipments of liquefied natural gas, accounting for around 20% of global consumption, within the waters of the Arabian Gulf. As a result, international energy markets are experiencing sharp price volatility affecting Brent crude futures and European gas contracts.

At the same time, maritime shipping lines have been compelled to reroute their commercial fleets, forcing them to navigate around the historic Cape of Good Hope route at the southern tip of Africa. This enforced geographic diversion adds approximately 19 days to maritime transit times to and from Asia, generating weekly losses for global supply chains estimated at between $2 billion and $3 billion in additional operating and fuel costs.

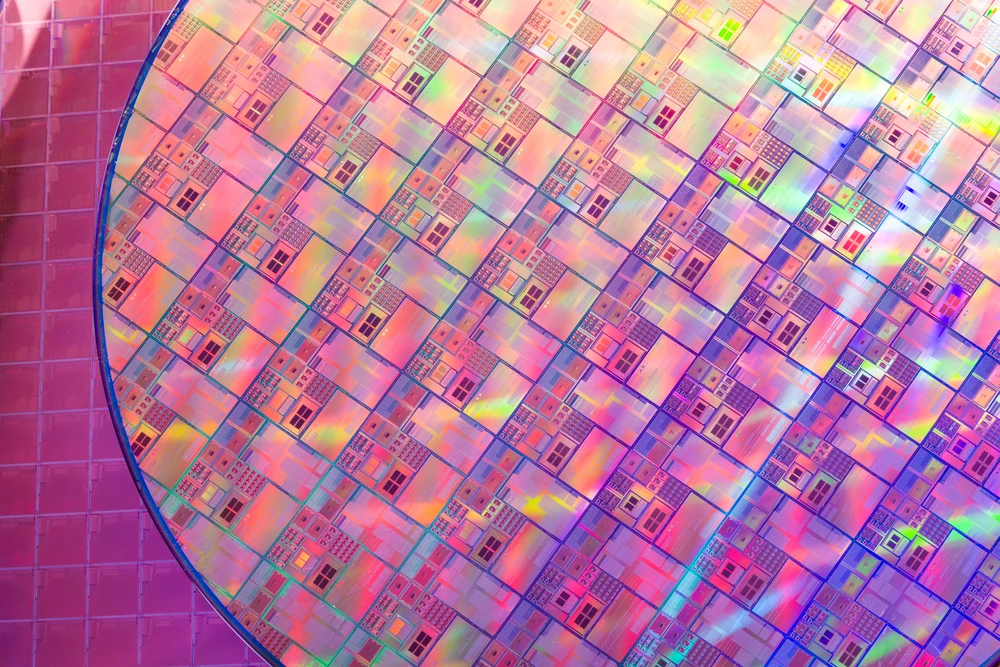

This operational disruption directly affects the technological infrastructure of East Asia, where advanced semiconductor fabrication facilities in Taiwan and South Korea require vast, continuous electricity supplies to operate lithography systems around the clock. These critical facilities, which account for approximately 68% of global semiconductor production, rely on imported liquefied natural gas to ensure the stability of their power networks and prevent disruptions.

In parallel, the precision manufacturing processes involved depend on highly specialised raw materials whose primary sources are concentrated in regions currently affected by the crisis. In particular, production lines require ultra-high-purity helium gas, extracted as a by-product from Gulf LNG liquefaction facilities, which represent roughly 35% of global supply, as well as bromine, which Korean factories import at a rate of 97.5% from the Dead Sea coast for chemical etching processes. Accordingly, technology firms are accelerating efforts to assess their exposure to the dual energy and critical chemical input shortages. At the same time, economic stakeholders monitor the crisis's trajectory with heightened caution to safeguard supply chain continuity.

Accordingly, this analysis examines the strategic and operational implications arising from the closure, focusing on three principal dimensions. First, it addresses the disruption of liquefied natural gas supplies and their direct impact on the security of power grids that sustain major Asian semiconductor manufacturing hubs. Second, it examines the sharp interruption in the supply of critical raw materials, particularly specialised gases and petrochemical inputs required for precision manufacturing processes. Finally, it explores the logistical repercussions of the forced rerouting of maritime shipping routes, as well as the strategic measures states are considering to mitigate future geopolitical risks.

Programmes

15 Mar 2026

Strait of Hormuz Closure: How Middle Eastern Crises Are Reshaping the Global Nuclear Energy Landscape

The United States and Israel launched Operation Epic Fury in late February 2026, targeting Iran’s nuclear and missile infrastructure and seeking to remove its political leadership. Although the operation achieved its initial tactical objectives with high precision, it provoked an asymmetric retaliatory response from the remaining Iranian forces. This response took the form of a comprehensive blockade of the Strait of Hormuz, the world’s most critical maritime artery for energy transport, triggering a severe global economic shock. Such disruption could propel the international system towards reducing its reliance on fossil fuels and accelerating the adoption of alternative domestic energy solutions, most notably nuclear power.

At the same time, global electricity demand is rising sharply, driven by the rapid expansion of advanced artificial intelligence infrastructure and high-performance computing facilities. This sudden disruption of fuel supplies places policymakers in major industrial economies under immediate economic and security pressures, while simultaneously exposing the profound consequences of closing the Strait. In this context, the present analysis examines the repercussions of the Strait of Hormuz's closure on global supply chains. It then develops a historical comparison with the oil price shocks of the 1970s, illustrating how those crises redirected states towards nuclear technology. The study concludes by analysing emerging regulatory and financial measures, as well as new geopolitical alignments, that are accelerating the global drive to construct nuclear reactors in 2026.

Programmes

10 Mar 2026

Where Does China Stand in the US-Israel-Iran War?

The U.S.-Israel and Iran War has affected the interests of many countries. In the last few days, China emerged as a significant player in these events. Beijing called for an immediate halt to the attacks by both sides and the protection of vessels passing through the Strait of Hormuz, culminating with the Chinese Foreign Minister Wang Yi pledging to send a special envoy to the Middle East for mediation.

Beijing has interconnected interests in the Middle East that are significantly affected by the war and will most likely reshape its strategic opportunities in the region, particularly in terms of energy security, trade routes, and diplomatic relations with key regional players. Beijing’s pragmatic foreign policy approach toward the region relies on protecting its economic interests and maintaining a strategic balance. So, the war could provide an opportunity for China to navigate new opportunities in the region and, consequently, expand its influence, particularly by strengthening ties with other oil-producing nations and increasing its investments in reconstruction efforts.

Likewise, China’s strategic partnership with Iran mainly revolves around oil supply and large-scale investments. The consequences of the war raise questions about the future of this relationship and the possibility that China may reshape its foreign policy toward Tehran if it faces a potential decline in Iran’s ability to sustain such interests as a result of the strain on its power after the war.

Publications

2 Mar 2026

Deterrence Gap: Will the Eastern Shield Secure Tehran’s Airspace in the Next Confrontation?

The military operations that unfolded over twelve days in June 2025 between Iran and Israel marked a sharp breakpoint in the trajectory of regional military balance. The confrontation resulted in a substantial erosion of Tehran’s military infrastructure and inflicted significant material losses. The depth of this operational failure was most evident in the near-total collapse of Iran’s integrated air-defence system, with confirmed intelligence assessments indicating that Israel succeeded in neutralising more than 80 surface-to-air missile batteries and destroying over 120 launch platforms. This effectively stripped Iranian airspace of its protective shield and imposed a state of absolute Israeli air superiority.

Amid this collapse, Tehran effectively lost its entire arsenal of the Russian-made S-300PMU2 (“S-300 PMU-2”) systems, which it had acquired in 2016 after protracted negotiations and at considerable financial cost. These systems were systematically destroyed between 2024 and 2025. Iran’s domestic air-defence industries, represented by the Bavar-373 and Khordad-15 systems, also demonstrated clear operational inadequacy when tested in a real combat environment.

This exposed a wide technological gap between Israel’s offensive capabilities and Iran’s defensive assets. The Iranian air-defence network failed to record the downing of a single manned Israeli fighter jet, and Iran’s ageing air force, reliant on pre-revolution legacy aircraft such as the F-14 Tomcat, the Phantom, and the Tiger, supplemented by 1990s-era MiG-29s, stood incapable of competing or deterring effectively.

This total inability to contest the battlespace not only underscored tactical failure but delivered a decisive blow to the strategic assumptions underpinning Iran’s defence doctrine for decades, particularly its reliance on “asymmetric missile deterrence” and hybrid layered-defence networks.

Confronted with a reality in which its missile capabilities were neutralised and its aerial shield dismantled, the Iranian leadership was compelled to adopt a “post-war reset” strategy, launching an urgent acquisition campaign aimed at closing the technological gap by turning eastward towards Russia and China to rebuild its lost deterrence.

The fundamental question that will shape the next phase in the Middle East remains: Can this “hybrid deterrence”, comprising domestic missiles alongside imported, only partially integrated weapon systems, endure against an adversary that has already demonstrated both the willingness and the capability to deliver devastating strikes deep inside Iran?

Programmes

20 Feb 2026

China’s Tariff-Exemption Policy for Africa: Drivers and Outcomes

The Chinese Government, on Feb. 14, 2026, issued decisions abolishing 100% of customs duties on exports from 53 African countries. This step marks a significant shift in the trajectory of Beijing’s historic relationship with the African continent. This relationship began 70 years ago with major infrastructure ventures such as the construction of the Tazara Railway in the 1970s. It gradually evolved into an increasingly intricate framework of reciprocal economic integration.

This evolution has been reflected in the substantial expansion of bilateral trade, which reached a historic high of USD 348.1 billion in 2025, with annual growth of 17.7%. Through this new tariff-exemption framework, Beijing is voluntarily relinquishing approximately USD 1.4 billion in annual customs revenue upon the regime’s implementation, a move that constitutes a long-term geoeconomic investment aimed at reinforcing the stability of supply chains. This shift may reshape the global trade landscape and further position the African continent at the centre of intensifying competition for industrial resources and clean-energy technologies.

Accordingly, this analysis examines the strategic dimensions of this new trade regime by focusing on the updated structural dynamics of bilateral trade and their actual impact on Africa’s trade balance; the global competition to secure supply chains for critical minerals and the resulting implications for local industrialisation ambitions; and, finally, an assessment of the countervailing economic and political strategies adopted by Western blocs as they seek to reposition themselves and respond to expanding influence across the continent.

Programmes

11 Feb 2026

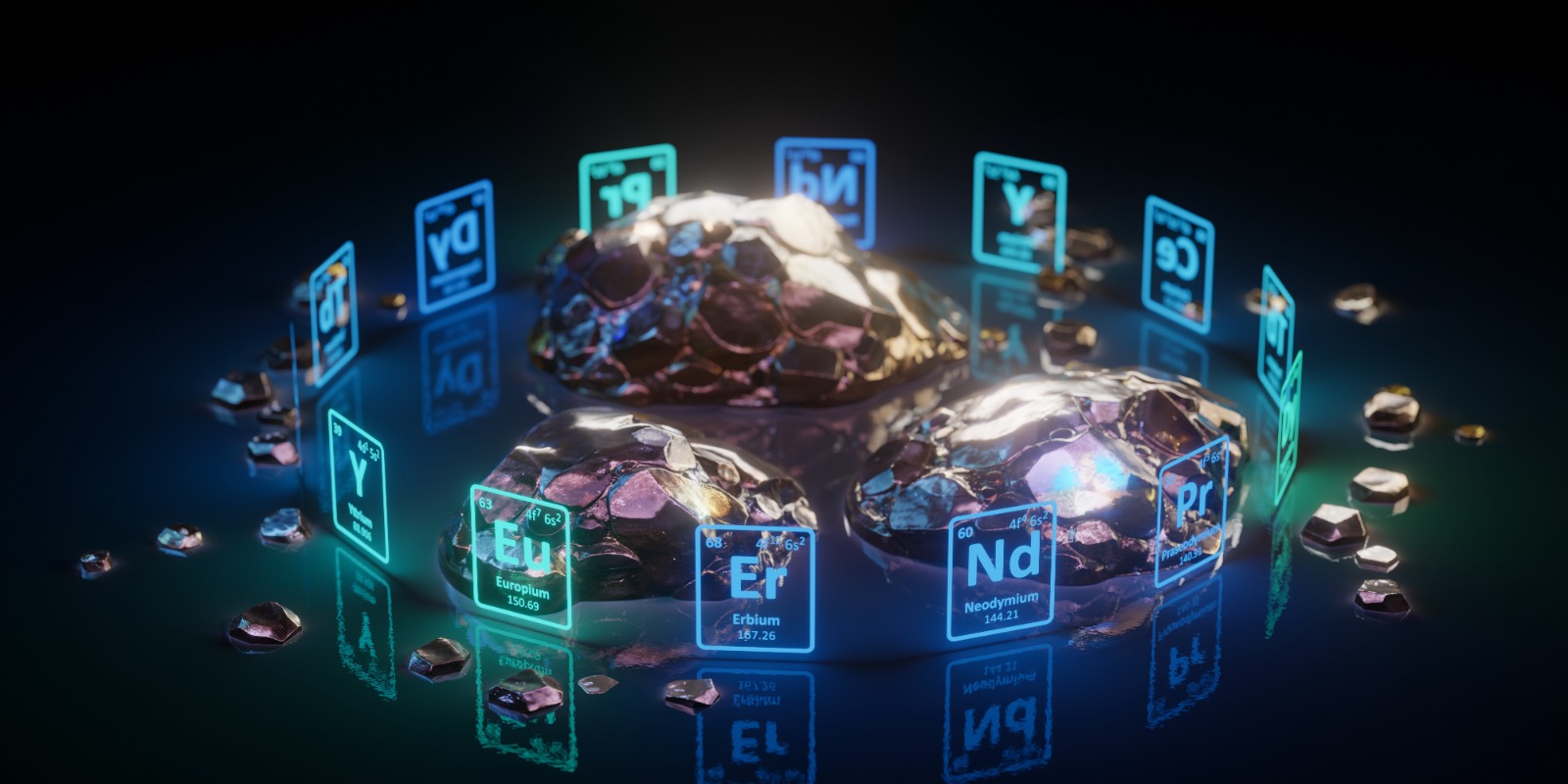

The GCC and the Future of the Rare Earths and Critical Minerals Race

China is a dominant player in the rare earths and critical minerals industry. As of 2025, China is in control of “…about 61% of rare earth production and 92% of their processing”, meaning China monopolized the rare earths and critical minerals industry. While China dominates this industry, countries have been aiming to bolster their own rare earth and critical mineral ambitions to reduce their reliance on China as a supplier of raw materials and processed products. For example, GCC countries, in line with their 2030 visions, have increased their investments in the mining and processing of these elements to diversify their economies and become suppliers in an industry dominated by China. This analysis aims to assess the emergence of the GCC as a rare earths and critical minerals supplier, which will be done by analyzing the reasons and feasibility for GCC involvement in this industry as well as understanding the challenges these countries face in their entry into the market.

Programmes

7 Feb 2026

Transformations in the Uranium Enrichment Market and the Future of Global Energy

Since 2023, the uranium enrichment market has undergone its most profound structural transformation since the advent of the civilian nuclear era. After three decades characterised by persistent oversupply and the integration of Russian inventories with Western reactor fleets, the sector, valued at approximately $15.5 billion in 2025, now confronts a fundamentally altered geopolitical landscape. stems primarily from the fact that nearly 95% of global enrichment capacity is controlled by just four entities, placing Western supply chains under complex logistical and political pressures.

Central to this transformation is the evolution of what is known as the Separative Work Unit (SWU) from a readily available commodity into a strategic bottleneck capable of redrawing global energy maps. The market has shifted rapidly from a buyer-dominated structure to one characterised by seller leverage, amid an intensifying race to secure fuel for both conventional reactors and small modular reactors (SMRs), which require advanced uranium grades for which Western markets lack adequate commercial infrastructure.

Accordingly, this analysis explores the contours of the new enrichment landscape, examining the principal actors and evolving pricing dynamics, while projecting the profound implications of this transformation for global energy security.

Programmes

22 Jan 2026

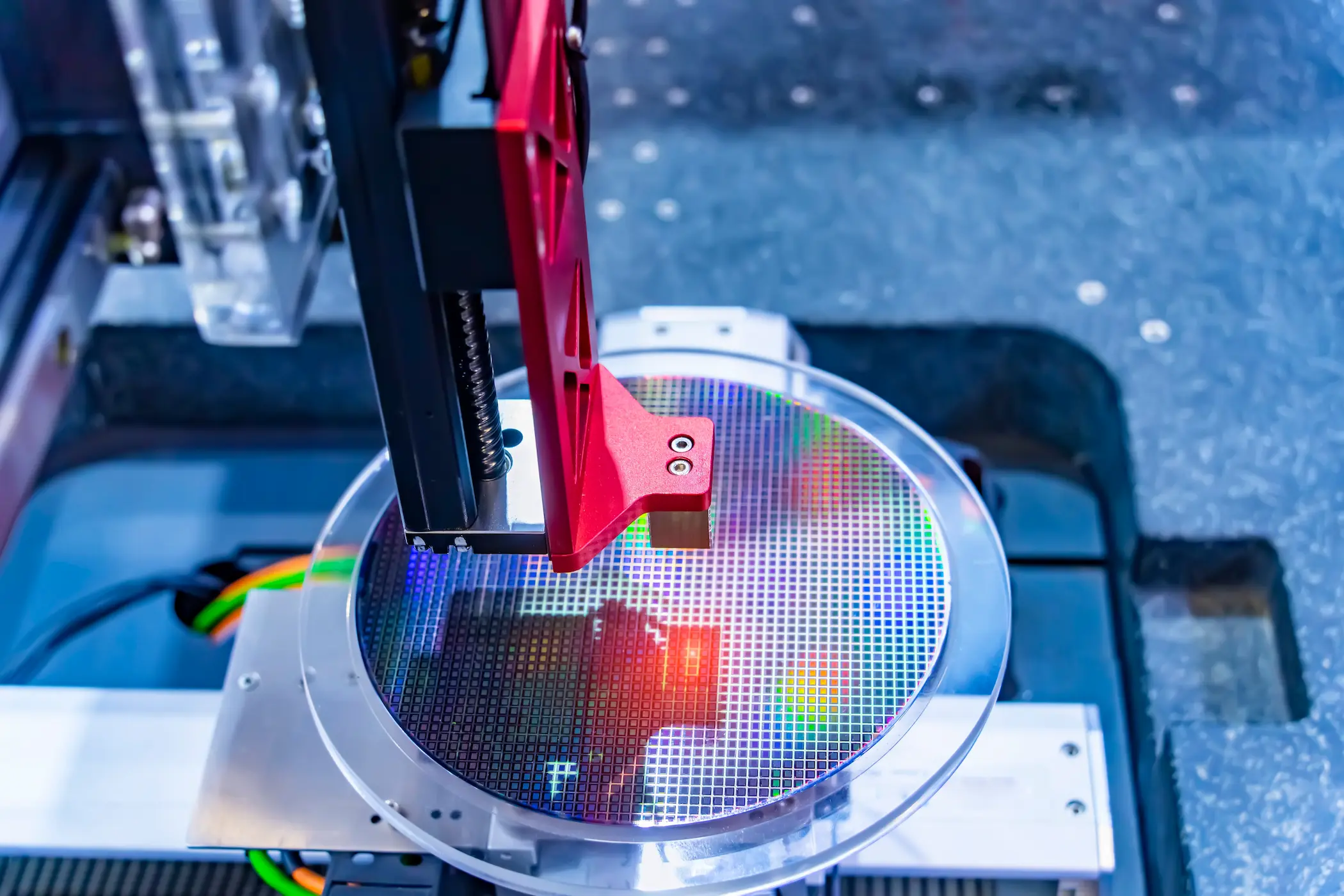

The Implications of China’s Acquisition of a Lithography System

December 2025 marked a structural shift in the global technological balance of power, as a state-backed Chinese industrial consortium, coordinated by Huawei, approved the operation of a functional prototype of an extreme ultraviolet (EUV) lithography system at a facility in Shenzhen. This announcement dismantles a core assumption that has dominated geopolitical thinking in Washington, Brussels, and Tokyo over the past decade, namely that the extreme engineering complexity of EUV technology would permanently confine China behind a technological barrier, preventing it from advancing beyond the 7-nanometre threshold in leading-edge semiconductor manufacturing.

Western containment strategies were grounded in a firm conviction that the Dutch firm ASML’s monopoly over highly complex supply chains would guarantee the exclusion of the world’s second-largest economy from producing the advanced semiconductors required for artificial intelligence applications. The new Chinese prototype, however, has invalidated this assumption, not by replicating Western engineering paradigms, but by pursuing an alternative physical and engineering pathway, shaped by imperatives of national sovereignty and enabled by effectively unconstrained state capital.

This prototype, based on laser-driven plasma (LDP) technology, demonstrates that Chinese engineering teams have mastered the core physical principles of optical control at 13.5 nanometres. In doing so, they have moved beyond a phase long framed as one of "scientific impossibility", shifting the contest decisively into a new stage defined by engineering scale-up and operational viability. This development signals the end of an era of unipolar technological dominance. It inaugurates a new phase of dual ecosystems within the semiconductor industry. This transformation will require a comprehensive reassessment of the economic and security assumptions that have governed the sector for decades.

Programmes

12 Jan 2026

The Collapse of the Western Flank: The Implications of Maduro’s Fall for Iran

Operation Absolute Resolve, which resulted in the removal of Nicolás Maduro and his spouse Cilia Flores on Jan. 3, 2026, constituted a watershed moment in the history of 21st-century geopolitical warfare. While initial indicators point to a seemingly limited regime change within Venezuela, the strategic repercussions of the operation inflicted severe damage on Iran’s forward-operating capabilities. For nearly two decades, Venezuela was not merely a diplomatic partner of Tehran; it served as an indispensable logistical bridgehead and a secure sanctuary in the Western Hemisphere. Through this platform, the Iranian regime was able to circumvent international sanctions, project asymmetric influence, and sustain a critical financial lifeline through illicit trade.