Rare earth elements (REEs) are a group of 17 elements that are crucial for the production of a wide range of high-tech products. Ironically, REEs are not “rare” and are found abundantly throughout the world, however, when found they are in such low concentrations that extraction is not feasible. Furthermore, when found in higher concentrations they must be separated from other elements, a process that is both environmentally and financially costly.

REEs are vital for several industries and are used in electronics, military technology, and most importantly, renewable energy. Although substitutes exist for REEs with producers attempting to replace them, REEs continue to be more effective, therefore, given their importance in the production of renewable technologies such as wind turbines and electric vehicles, demand is expected to increase, with the European Union (EU) alone expecting REEs needs to increase fivefold as it and the rest of the world transitions to net-zero.

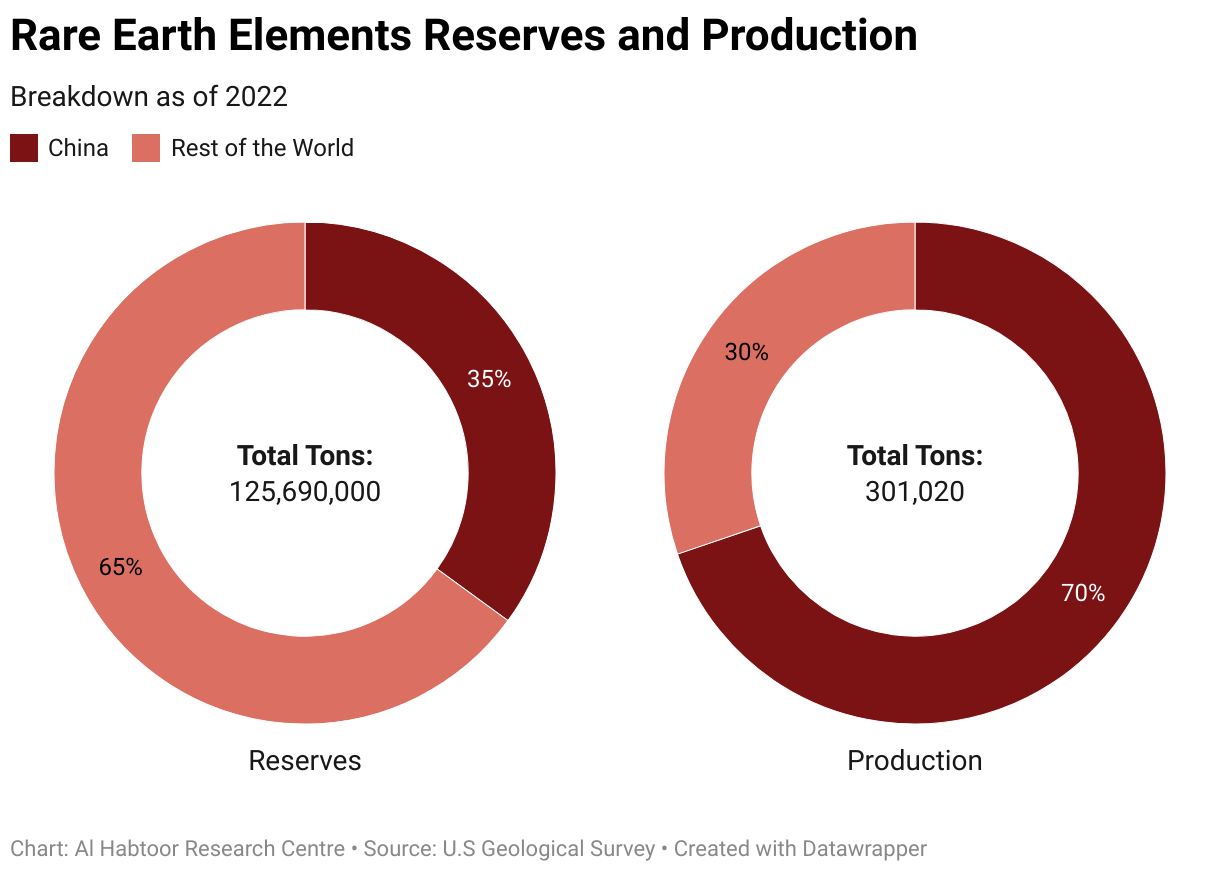

Currently, China dominates the global REEs market, accounting for over 35% of the world’s REEs reserves and 70% of production. China's domination of the REEs market has raised concerns over supply chain security, dependence on China, and China’s use of REEs as a political bargaining piece; such as when it cut exports to Japan following the arrest of a Chinese sailor by Japan. Recently, discoveries of REE deposits in Norway and Sweden have made headlines. The discoveries could have the potential to disrupt the market and have far-reaching implications.

Rare Earth Elements: Past and Present

In the 1950s and 1960s, the United States of America (USA) was the dominant producer of REEs with all of its demand being met at the Mountain Pass mine in California, but China emerged as a major producer in the 1990s due to multiple reasons.

Firstly, China has lower labour costs and more relaxed regulations, coupled with a slew of free-trade agreements with the USA, China quickly rose as a cheaper alternative to the USA. Secondly, China created processing facilities in close proximity to REEs mines further reducing costs, while also expanding their manufacturing of electronics to take advantage of their abundance of REEs. Finally, the Mountain Pass mine was unable to compete with China, new, stricter regulations were passed in the USA, and pollution of the surrounding areas water supply led to the shutdown of the Mountain Pass mine, America’s only source of REEs.

Over the next three decades, China became the dominant producer of REEs, accounting for 70% of global production in 2022. It has not limited its efforts to control the REEs market with its domestic resources. It has spread its influence to Africa in resource rich countries such as the Democratic Republic of Congo, Kenya, and Tanzania. It has also targeted Latin America with a particular focus on Brazil as it has significant REEs reserves.

China’s dominance of the REEs market, its decisions to halt exports in 2010, and the importance of REEs to the defence and renewable energy industries, has led to concerns about supply chain security and dependence on China for critical elements, and has prompted governments and companies around the world to seek alternative sources of REEs. The USA reopened the Mountain Pass mine in 2012 and announced new mining and processing projects across the country which has increased its share in global production to 14%. Australia’s Lynas Corporation has also become a major western producer and has received funding from the USA to build processing facilities.

In recent years, new REE extraction projects have been developed in a number of countries, including Australia, Canada, and Russia. More recently Sweden announced it had discovered the largest deposit of REEs in the EU and Norway followed with its own announcement of a significant REEs deposit on its seabed. These new sources of REEs have the potential to reduce dependence on China and improve supply chain security, but many challenges remain, including the high cost of production, environmental concerns, and the complex nature of REE extraction.

What is it Good for? Absolutely Everything!

Rare earth minerals have unique magnetic, conductive, and luminous properties, which has made them increasingly essential for a variety of high-tech applications. They are used to create permanent magnets in wind turbines and robotics, traction motors in electric vehicles, and fuel cells for hydrogen energy. Furthermore, they are critical to a wide range of applications in the defence industry with an estimated 420 kgs of REEs needed to manufacture a single F-35 Lightning II with REEs being used in electro-optical systems, sensors, and electronics. In addition, they play a critical role in the development of clean energy technologies, including solar panels, hybrid vehicles, and energy-efficient lighting.

Although there are substitutes available for REEs, they are less efficient with producers opting to continuing their reliance on REEs. Given its current importance in the defence industry and its current and future importance in the transition to net-zero, REEs are a critical resource and the control of said resource by one country can be both a national security risk and an energy risk.

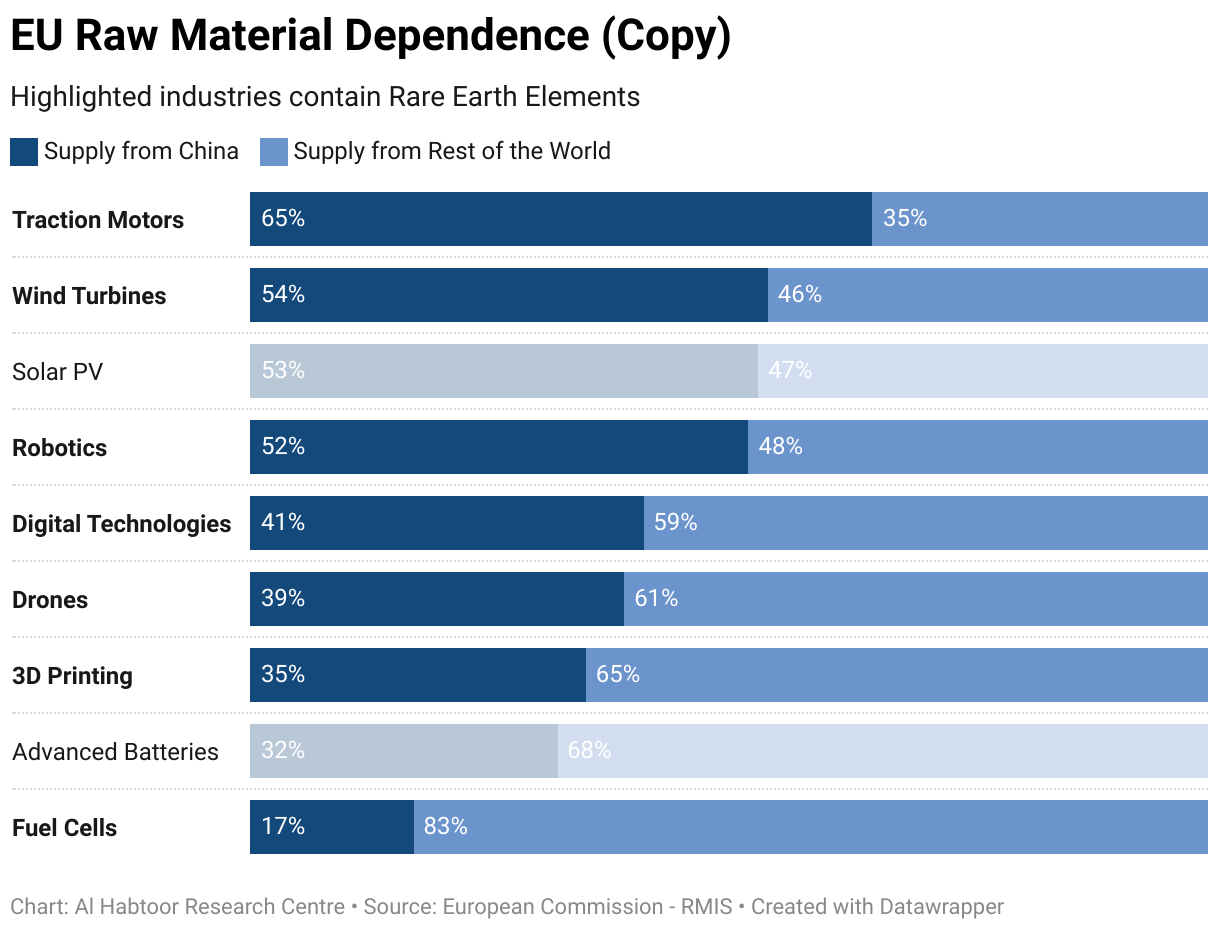

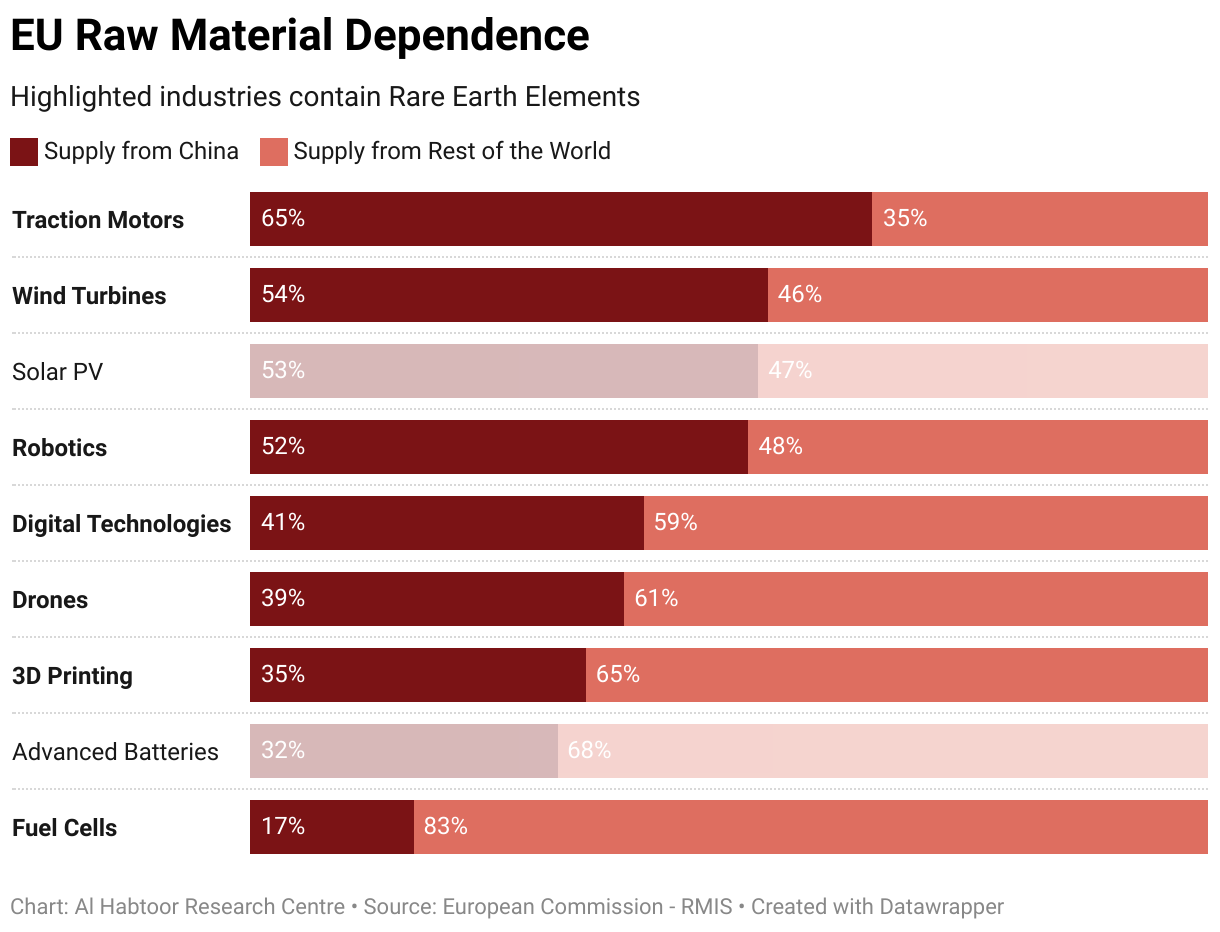

Following the Russia-Ukraine War the majority of the EU realised the cost of their dependence on Russian energy sources and exposed weaknesses in the defence industry, these shocks pushed the EU to fasten its transition to clean energy and address shortcomings in its military supply chain. As discussed previously REEs play a vital role in both industries and in 2020 EU imported between 98-99% of its REEs from China, those REEs are vital in a number of strategic industries.

The reliance on a single country for vital goods mirrors the EUs previous dependence on Russian energy, given the expectation that demand for REEs will increase fivefold in the EU the recent discoveries in Sweden and Norway can have serious implications for the future of the REEs market.

Implications of New Discoveries Outside China

The discovery of the EUs largest reserve of REEs in Sweden which was quickly followed by another significant discovery in Norway caused speculation about a possible shift in the global REEs balance as the USA and the EU aim to be less dependent on China. Generally, the discovery of new REEs in countries outside China’s sphere of influence carry a number of implications.

Firstly, competition in the REEs market would increase, leading to lower prices and more availability to consumers. REEs that are available at cheaper prices will encourage clean energy innovation and in theory lower prices which could speed up the world’s transition to net-zero. Secondly, diversified sources of REEs would reduce reliance on China and lower risks to supply chain disruptions such as those that occurred in 2010 and 2019. Finally, the expansion of extraction and processing in countries with stricter environmental regulations may push producers in those countries to introduce new technologies, that increase extraction efficiency and lower the impact that mining REEs has on the environment.

The discovery in Sweden is estimated at over 1 million tons, or 0.8% of global reserves. Although the reserves are small compared to China’s 44 million tons, a relatively small number of REEs is extracted every year. Therefore, the discovery can have a significant impact on the EU and its goals of diversifying its sources of REEs and it would be the continents first significant source of REEs. However, it is expected that it will take 10-15 years before extraction at the mine commences and if it does so, changes in the market could make the project unfeasible.

Norway’s discovery is more complicated as the deposits exist on the seabed, making extraction prohibitively complicated and expensive, furthermore, environmental regulations are stricter in the Scandinavian country and extraction may not occur if it proves detrimental to the surrounding ecosystem. Should the mines become active they will be sufficient to meet a large part of the EU’s future demand of REEs, however, there is still a long way to go before we may see an impact. Furthermore, given China’s monopoly on REEs and its more relaxed regulations, it may simply increase production quotas to drive down prices and make it economically unfeasible to continue mining projects in the EU, which would maintain the EUs dependence on China for increasingly vital raw materials.

In conclusion, developing new sources of REEs is a challenging and expensive process, and the full impact of new discoveries will depend on a variety of factors; the size of the deposit, the feasibility of extraction and processing, the consumers’ appetite to pay potentially higher prices for REEs, and the willingness of residents to bear the environmental damage caused by their extraction.

References

Adomaitis, N. (2023, January 27). Norway finds ‘substantial’ mineral resources on its seabed. Reuters. Retrieved February 13, 2023, from https://www.reuters.com/markets/commodities/norway-finds-substantial-mineral-resources-its-seabed-2023-01-27/

Bradsher, K. (2010, September 23). Amid tension, China blocks vital exports to Japan. The New York Times. Retrieved February 16, 2023, from https://www.nytimes.com/2010/09/23/business/global/23rare.html

Breton, T. (2022, September 14). Critical Raw Materials Act: securing the new gas & oil at the heart of our economy. European Commission. Retrieved February 15, 2023, from https://ec.europa.eu/commission/presscorner/detail/en/STATEMENT_22_5523

Chatterjee, P. (2023, January 12). Huge Rare Earth Metals Discovery in Arctic Sweden. BBC News. Retrieved February 12, 2023, from https://www.bbc.com/news/world-europe-64253708

Critical Raw Materials Resilience: Charting a Path towards greater Security and Sustainability. European Commission. (2020, September 3). Retrieved February 15, 2023, from https://eur-lex.europa.eu/legal-content/EN/TXT/HTML/?uri=CELEX%3A52020DC0474&from=EN

Europe’s largest deposit of rare earth metals is located in the Kiruna Area. LKAB. (2023, January 12). Retrieved February 15, 2023, from https://lkab.com/en/press/europes-largest-deposit-of-rare-earth-metals-is-located-in-the-kiruna-area/

Parman, R. (2019, September 26). An Elemental Issue. www.army.mil. Retrieved February 15, 2023, from https://www.army.mil/article/227715/an_elemental_issue

U.S. Geological Survey, Mineral Commodity Summaries, January 2023

4

4

3

3

Related Articles

Rise of Medical Robotics Market: What About Safety?

Interview with ChatGPT: Will These Applications Bring the End of Human Knowledge?

Hey Siri, Build a House: 3D Printing in Construction

Ramifications for the Global Economy in the Case of a China-Taiwan Conflict?

The Militarisation of European Politics

Sports Diplomacy and the Reduction of Global Political Tensions

What If: The UN Runs Out of Money?

What If: China Invades Taiwan?

TikTok: China’s New Weapon

Rescheduling: Prioritising Arms over Development on the European Parliament’s Agenda

Comments