Since 2023, the uranium enrichment market has undergone its most profound structural transformation since the advent of the civilian nuclear era. After three decades characterised by persistent oversupply and the integration of Russian inventories with Western reactor fleets, the sector, valued at approximately $15.5 billion in 2025, now confronts a fundamentally altered geopolitical landscape. stems primarily from the fact that nearly 95% of global enrichment capacity is controlled by just four entities, placing Western supply chains under complex logistical and political pressures.

Central to this transformation is the evolution of what is known as the Separative Work Unit (SWU) from a readily available commodity into a strategic bottleneck capable of redrawing global energy maps. The market has shifted rapidly from a buyer-dominated structure to one characterised by seller leverage, amid an intensifying race to secure fuel for both conventional reactors and small modular reactors (SMRs), which require advanced uranium grades for which Western markets lack adequate commercial infrastructure.

Accordingly, this analysis explores the contours of the new enrichment landscape, examining the principal actors and evolving pricing dynamics, while projecting the profound implications of this transformation for global energy security.

Economic Determinants and Technological Shifts in Uranium Enrichment

A comprehensive understanding of the current structural transformation requires first examining the underlying physical and economic foundations of the enrichment industry. The core value of this market lies not merely in the raw material itself, but in the complex industrial service required to convert it into reactor-grade fuel. Light-water reactors, which constitute the backbone of the global nuclear fleet, depend on increasing the concentration of the fissile uranium isotope (U-235) from its naturally occurring level of approximately 0.7% to between 3% and 5%.

This process is not traded as the sale of a simple commodity, but rather as a specialised service measured in SWUs. From an engineering perspective, the SWU quantifies the amount of effort and energy required to separate feed material into two distinct streams: enriched product suitable for fuel fabrication, and depleted residual material known as Tails.

The reciprocal relationship between natural uranium feedstock and enrichment effort is governed by a critical operational variable known as the tails assay, which provides operators with strategic flexibility in resource management.

Over the past three decades, the relative abundance and low cost of enrichment capacity enabled operators to pursue an “Underfeeding” strategy. In practice, this meant expending greater separative work to extract the maximum possible share of fissile isotopes from each unit of feed material. The result was a substantial reduction in natural uranium requirements and the creation of what became known as a “Virtual Mine,” effectively injecting nearly 6,000 tonnes of uranium equivalent annually into the global market.

The current landscape, however, reflects a profound reversal toward an “overfeeding” strategy, driven by the scarcity of enrichment capacity in Western facilities. Operators are now compelled to reduce the separative effort expended and accelerate production cycles, even at the cost of leaving higher concentrations of uranium in the tails. This shift inevitably results in greater volumes of natural uranium being consumed to produce the same quantity of enriched fuel, thereby transferring the pressures of shortage and constraint from the industrial enrichment segment to the upstream mining sector.

These economic dynamics have been accompanied by decisive technological shifts that have redefined the industry’s cost structure. The transition from the era of gaseous diffusion, characterised by extraordinarily high energy consumption of roughly 2,500 kilowatt-hours per separative work unit and a direct linkage between enrichment costs and electricity prices, to the dominance of “Gas Centrifuge Technology” marks a structural turning point. Today, centrifuge-based systems account for approximately 58.9% of global enrichment capacity.

Gas centrifuges have reduced energy consumption by a factor of fifty, lowering requirements to roughly 50 kilowatt-hours per separative work unit. These dramatic efficiency gains effectively severed the historical linkage between fuel costs and electricity prices. The financial burden has consequently shifted from operational energy expenditure to substantial capital outlays, particularly for the precision manufacture and installation of ultra-high-speed rotors capable of operating at supersonic velocities continuously for years without interruption.

This strategic market is currently valued between $13.8 billion and $15.5 billion, with strong growth projections reflecting a fundamental repricing of enrichment as a security-sensitive asset. For many years, the sector operated under sustained price suppression and a gradual erosion of Western industrial capacity, largely as a consequence of the “Megatons to Megawatts” programme, which ran until 2013. Under this arrangement, surplus Russian nuclear warheads were down-blended into reactor fuel for the U.S., at one point supplying approximately 50% of US demand.

While the programme delivered short-term supply stability and cost advantages, it simultaneously contributed to the contraction of Western enrichment infrastructure, creating the structural void that markets are now striving to fill within a far more complex geopolitical environment. The following figure illustrates the market’s evolution and projected growth trajectory for 2014–2030.

The Geography of Dominance and the Balance Among the Four Major Players

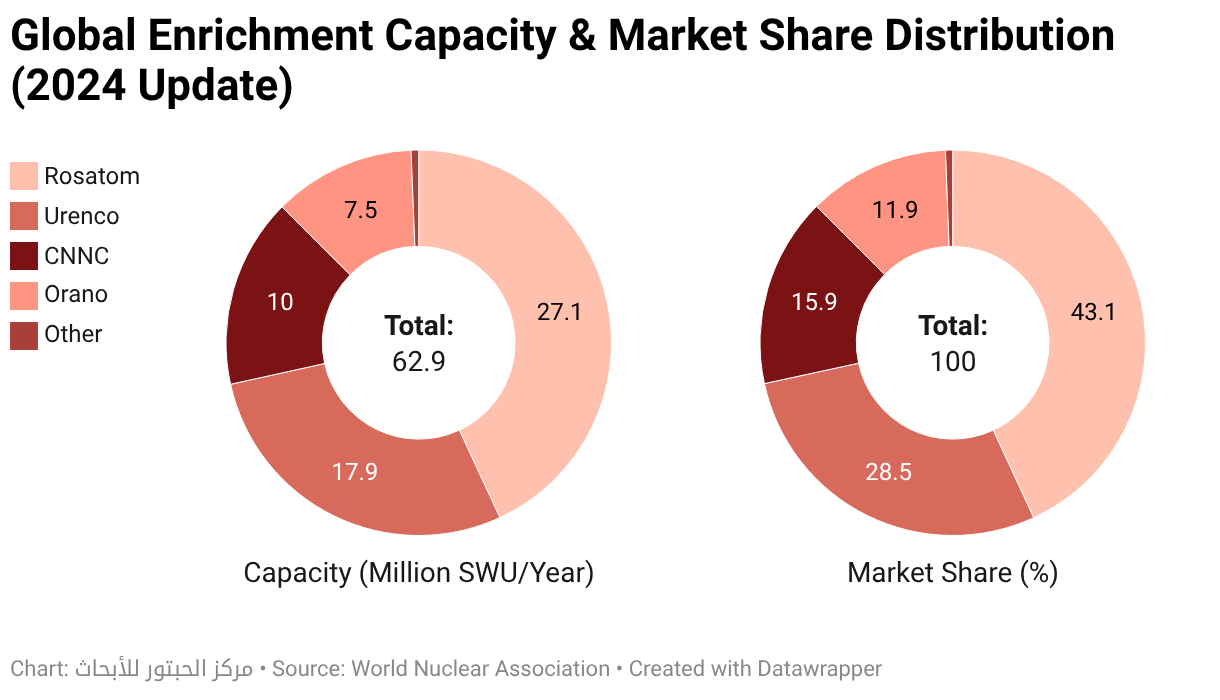

These intricate physical and economic determinants are inseparable from the institutional architecture that governs them. The capital intensity and formidable technological barriers inherent in uranium enrichment have produced a market structure characterised by oligopoly. Just four entities control approximately 95% of global commercial enrichment capacity, making this extreme concentration the fundamental source of current supply chain fragility.

At the apex of this hierarchy stands Russia’s state nuclear corporation, Rosatom, which commands a dominant 44% share of global capacity, equivalent to roughly 27.1 million SWUs. This position is underpinned by vast industrial complexes inherited from the Soviet era, including facilities such as Zelenogorsk and Novouralsk. Yet Rosatom operates not merely as a conventional commercial enterprise; it functions as a vertically integrated instrument of geopolitical influence. By offering reactors, financing, and fuel supply as a bundled package to emerging economies, the corporation has sustained export flows and demonstrated resilience against Western sanctions, particularly by redirecting shipments toward alternative, non-aligned markets in the aftermath of the Russia-Ukraine war.

The following figure outlines the production capacities and market shares of the four dominant players in the global enrichment landscape.

By contrast, the Urenco consortium stands as the principal Western competitor and the foremost counterweight to Russian dominance, with an enrichment capacity of approximately 17.9 million SWUs. Distinctively, Urenco operates as a multinational entity, managing facilities in the United Kingdom, the Netherlands, and Germany, as well as the URENCO USA plant in New Mexico. The latter holds particular strategic significance as the only currently operating commercial enrichment facility on U.S. territory.

Urenco is spearheading Western efforts to restore market equilibrium through an ambitious expansion programme designed to add 2.5 million SWUs of capacity by 2030. The initiative focuses on expanding operations at its Almelo facility in the Netherlands and scaling up production in the US to address the anticipated structural supply deficit in the coming years.

These efforts are complemented by the strategic positioning of Orano, a central pillar of France’s energy sovereignty. The company operates the Georges Besse II enrichment plant, with a capacity of approximately 7.5 million SWUs. In response to geopolitical disruptions and the curtailment of Russian supply flows to Europe, Orano has launched a project to increase its capacity by 30%.

At the same time, the company is pursuing a return to the U.S. market, having selected Oak Ridge, Tennessee, as the proposed site for a new enrichment facility. If realised, the project would significantly reinforce domestic US enrichment infrastructure during the 2030s.

This already intricate landscape is further shaped by the rapid ascent of the China National Nuclear Corporation (CNNC), which is transitioning from a strategy centred on domestic self-sufficiency to an increasingly influential role in global enrichment trade. China is targeting an enrichment capacity of approximately 17 million SWUs by 2030, positioning itself as a major structural player in the market.

Beijing’s manoeuvres have generated strategic concern in Western capitals, where they are viewed as a potential conduit for the indirect re-entry of Russian enriched uranium into Western markets. Under this dynamic, China imports Russian-enriched material for use in its domestic reactor fleet while exporting its own enrichment output abroad. The result is a complex substitution mechanism that may allow Russian-origin supply to continue reaching Western markets indirectly through layered commercial exchanges.

Transformations in Global Demand and the Politicisation of the Market

This pronounced concentration on the supply side is generating parallel and structural shifts in demand behaviour. The buyer base is composed primarily of public utilities, particularly state-owned electricity companies, whose exposure to operational risk is exceptionally acute. Although fuel costs typically account for only 5–10% of total operating expenditures, even a minor disruption in supply can result in a complete halt to generation and the loss of 100% of revenues.

Accordingly, major global actors such as Constellation Energy and EDF have definitively abandoned the “just-in-time” import model that prevailed over the past decade. In its place, they are moving decisively toward the accumulation of substantial strategic inventories designed to ensure operational continuity for years to come, prioritising the security of supply over incremental cost savings.

Demand patterns also diverge sharply across regions, reflecting the geopolitical realities shaping each market. The U.S., which possesses the world’s largest nuclear generation capacity, faces a strategic predicament stemming from its longstanding dependence on imports. Projections point to an annual shortfall exceeding 11 million pounds of uranium equivalent by 2028, a gap that has driven futures prices to record levels, averaging $97.66 per SWU in 2024.

Meanwhile, Western European states are seeking to decouple from Russia by diversifying supply sources. By contrast, Eastern European countries that remain technologically dependent on Russian-designed VVER reactors are effectively trapped in a pattern of structural reliance. At the same time, the Asia-Pacific region has emerged as the principal engine of global demand growth, driven by China’s expansive reactor construction programme and the renewed nuclear expansion strategies of Japan and South Korea.

This already complex equation is further compounded by rising energy consumption from the technology sector. Major corporations such as Amazon and Google have entered into direct negotiations with nuclear utilities to secure carbon-free baseload power for artificial intelligence data centres through long-term power purchase agreements, thereby intensifying tightness in forward markets.

In parallel, the emergence of next-generation SMRs introduces an additional structural challenge. These systems require an advanced fuel known as high-assay low-enriched uranium (HALEU), whose commercial production remains overwhelmingly concentrated in Russia. Consequently, the trajectory of Western nuclear innovation is increasingly contingent on its capacity to break this near-monopoly and establish parallel supply chains before strategic constraints become entrenched.

These shifts in buyer behaviour have not remained confined to abstract economic calculations. Instead, they have collided with geopolitical realities that have fully politicised the sector. The illusion of a unified global market has fractured, giving way to two distinct and increasingly segregated trading systems.

This division became particularly evident when the U.S. enacted the Prohibiting Russian Uranium Imports Act in May 2024, in response to vulnerabilities exposed by the war in Ukraine. Yet lawmakers were confronted with the structural reality that the U.S. relied on Russia for approximately 24% of its enrichment services. As a result, the legislation incorporated a system of waivers extending until early 2028.

This timeline has created a critical transitional phase. U.S. utilities continue to procure Russian material under legally sanctioned exemptions, while simultaneously racing to secure long-term contracts with Western suppliers for the post-2028 period. Moscow, for its part, responded with reciprocal escalation, imposing temporary export restrictions in November 2024, plunging the market into renewed cycles of price volatility.

Amid this escalating contest, China has emerged as a balancing actor adept at exploiting emerging trade gaps. Flow data for 2024 and 2025 indicate a pattern commonly described as “displacement exchanges,” whereby Beijing increases its imports of Russian enriched uranium to fuel its domestic reactors, thereby freeing national enrichment capacity, unconstrained by sanctions, for export to the United States.

This tactic enables China to assume the role of intermediary, thereby sustaining indirect supply to the U.S. market and substituting Chinese-enriched material for Russian-origin volumes in functional terms. Western lawmakers increasingly view this mechanism as a potential backdoor channel that may warrant future regulatory intervention, thereby adding further layers of risk to supply stability.

By contrast, Europe’s efforts to disengage have proven more complex and markedly slower than the U.S. push. Although the REPowerEU plan seeks to end reliance on Russian fuel by 2027, the European Union has refrained from imposing a comprehensive ban due to internal opposition from member states such as Hungary, which remains fully dependent on Russian technology at the Paks Nuclear Power Plant.

This structural dependency extends even to major nuclear powers such as France. Despite political commitments to diversification, French companies continue to engage with Rosatom, in part because Orano does not yet possess the technical capacity to reprocess recovered uranium (RepU) at comparable efficiency. Consequently, full decoupling remains a technically demanding and politically costly undertaking.

Five Inevitable Strategic Trajectories

The foregoing analysis points to five unavoidable strategic trajectories:

- Acute Structural Shortfall (2026–2028): Western markets are likely to confront a critical three- to four-year gap during which effective demand will exceed total non-Russian supply. This imbalance will compel temporary reliance on drawdowns from strategic inventories as an interim solution, pending the timely and flexible execution of capacity expansion plans led by Urenco and Orano to bridge this structural deficit.

- Entrenchment of Overfeeding and Amplified Upstream Demand: Persistent scarcity in SWUs will drive operators to institutionalise overfeeding as a durable operational strategy. This shift will structurally increase demand for natural uranium, thereby shifting bottleneck pressures upstream to the mining and conversion segments, as larger feedstock volumes become necessary to offset constrained enrichment capacity.

- Localisation of Value Chains and Structurally Higher Costs: The U.S. and Europe are now committed to an irreversible trajectory of rebuilding domestic fuel cycle capabilities. By 2030, this shift is likely to yield regionally anchored supply chains characterised by greater reliability and security. However, these systems will, by necessity, entail substantially higher capital and operating costs compared with the previous era of globally integrated, lower-cost procurement.

- The Technology Bet and the Fate of Small Modular Reactors: The pace and scale of SMRs deployment will hinge decisively on the West’s ability to establish independent production capacity for HALEU, alongside advances in laser enrichment technologies. Failure to break Russia’s near-monopoly over this specialised fuel would effectively constrain the ambitions of this next-generation reactor class, confining any prospective nuclear revival to large, conventional reactor designs.

- The End of the Unified Market and the Rise of the National Security Premium: The current fragmentation of the market is no longer a temporary disruption but has crystallised into a new structural baseline. The industry has shifted from a commoditised service sector to an arena of geopolitical contestation. The former “just-in-time” paradigm has been replaced by a “just-in-case” model, under which security of supply carries a discernible price premium. In this environment, strategic control over enrichment capacity has reasserted itself as a core pillar of national energy security.

In sum, this structural transformation is redefining the very concept of energy security in the 21st century. The nuclear fuel cycle can no longer be treated as a purely commercial domain governed by conventional supply-and-demand dynamics; it has evolved into a sovereign asset of strategic significance that is resistant to compromise.

Accordingly, the coming decade will be defined by a race to close the SWU gap. This contest will serve as a stringent test of Western alliances’ capacity to absorb the substantial economic costs and prolonged timelines required to achieve independence from Russian leverage.

As the contours of an emerging bipolar order take shape, pitting Western supply chains against an Eastern axis, the decisive Western wager rests on achieving technological breakthroughs, whether in laser enrichment or in developing independent HALEU supply chains. Without such advances, the anticipated nuclear renaissance risks becoming a casualty of geopolitical bottlenecks. Immediate investment in enrichment infrastructure, therefore, represents the only credible insurance policy for securing a sustainable future for carbon-free energy.

References

“Uranium Enrichment – World Nuclear Association.” 2025. World-Nuclear.org. 2025. https://world-nuclear.org/information-library/nuclear-fuel-cycle/conversion-enrichment-and-fabrication/uranium-enrichment.

“Uranium Markets Shake off Summer Doldrums.” 2026. Sprott.com. February 3, 2026. https://sprott.com/insights/uranium-markets-shake-off-summer-doldrums/.

Mordor Intelligence. 2025. “Uranium Enrichment Market Size, Share & 2030 Trends Report.” Mordor Intelligence. December 9, 2025. https://www.mordorintelligence.com/industry-reports/uranium-enrichment-market.

Market Research Future. 2024. “Uranium Enrichment Market Research Report — Global Forecast till 2035.” Marketresearchfuture.com. 2024. https://www.marketresearchfuture.com/reports/uranium-enrichment-market-29486.

“Uranium Market Size, Share, and Regional Trends.” 2024. Skyquestt.com. 2024. https://www.skyquestt.com/report/uranium-market.

Digges, Charles. 2024. “How Will the US Ban on Russian Enriched Uranium Impact Both Countries? – Bellona.org.” Bellona.org. May 30, 2024. https://bellona.org/news/nuclear-issues/2024-05-how-will-the-us-ban-russian-enriched-uranium-impact-both-countries.

“Russia Continues to Export Uranium to the United States.” 2025. OSW Centre for Eastern Studies. June 18, 2025. https://www.osw.waw.pl/en/publikacje/analyses/2025-06-18/russia-continues-to-export-uranium-to-united-states.

WorldNuclearNews. 2025. “Second Phase of US Enrichment Expansion Completed.” World Nuclear News. September 11, 2025. https://www.world-nuclear-news.org/articles/second-phase-of-us-enrichment-expansion-completed.

“Uranium Miners Lead Market Higher.” 2026. Sprottetfs.com. February 3, 2026. https://sprottetfs.com/insights/sprott-uranium-report-uranium-miners-lead-market-higher/.

“Uranium Marketing Annual Report – U.S. Energy Information Administration (EIA).” 2026. Eia.gov. 2026. https://www.eia.gov/uranium/marketing/.

“Small Modular Reactors – World Nuclear Association.” 2025. World-Nuclear.org. 2025. https://world-nuclear.org/information-library/nuclear-power-reactors/small-modular-reactors/small-modular-reactors.

“Roadmap to Fully End EU Dependency on Russian Energy.” 2025. European Commission. May 6, 2025. https://commission.europa.eu/news-and-media/news/roadmap-fully-end-eu-dependency-russian-energy-2025-05-06_en.

Related Articles

Middle East in Energy Transition: From Stopgap to Global Architect

Drums of War: Clean Energy Conflict on Both Sides of the Atlantic

The New Economics of Security: Priced for Permanence in a Fragmented World

Digital Sovereignty: A World Governed by Algorithms

The Collapse of Trust in the Digital State

Comments