Global trade tensions, supply chain disruptions, and skyrocketing costs are some of the unprecedented effects caused by U.S. president Donald Trump’s second term aggressive tariff policies. Tariff policies' impact goes beyond being just hypothetical, with real-time predictions and forecasts that more severe effects could follow; the global GDP is expected to slowly grow by only 2.2% in 2025, while the United Nations Conference on Trade and Development (UNCTAD) has warned of a possible global recession, given that growth slips below 2.5%. Not only the UNCTAD but also the International Monetary Fund (IMF) has downgraded its outlook for the global economy to 2.8% in 2025 and made a significant revision for the U.S. economy lowering its 2025 growth projection to 1.8% in April from 2.7% in January. Adding to these concerns, the World Trade Organization has already highlighted a sharp deterioration in global trade prospects, with world merchandise trade now expected to decline by 0.2% in 2025, nearly three percentage points lower than previous forecasts.

The current instabilities go beyond the economic aspect; they also affect the U.S.’s international alliances and add additional burdens to households, many of whom are delaying major life decisions. A pressing question amid recession fears arises: What are the impacts on a global scale in the event of a U.S. economic collapse? Given the leading position the U.S. plays as the world’s largest economy and the leading issuer of primary reserve currency, such a downturn would trigger a financial disaster of unparalleled magnitude. Essentially, if the U.S.’s economy falls, the world’s economy falls with it. Imagine waking up a few years from now, pulling out your phone, and seeing the headline: "U.S. Economy in Freefall: Markets Collapsed Overnight." It begins as a distant rumble, as if a story is taking place somewhere else. But then you go to get your morning coffee, and the price has tripled. Your investment app reveals that your life savings have been devastated. Overseas, factories that rely on American consumers come to a standstill, leaving entire villages jobless. The USD, once the cornerstone of global banking, has collapsed, provoking wild currency wars as governments try to preserve their own. Suddenly, that far-off catastrophe isn't so far away; it's emptying your wallet, increasing your grocery cost, and endangering your basic existence. This isn't just a headline; it's a chilling, global economic winter, its icy grip felt in every home, on every continent, for generations. Are we truly prepared for such a cataclysm?

Worrying Signs?

Ever since Donald Trump won the American elections, he promised a new wave of radical changes that would “Make America Great Again.” In fact, since assuming office last January, Trump in his second term has aggressively reinstated, expanded and implemented his tariff agenda, an agenda which led to unprecedented global tensions and instability in the trade sector, including disruption in supply chains, skyrocketing costs for multinational companies as well as spreading a state of uncertainty within global markets. Other factors affected ties and strategic alliances which have been greatly strained, as well as the implementation of retaliation measures from different nations. On the domestic level, the current agenda had its reflections on prices, which hiked, affecting both consumers and business owners, and wiped-out trillions USD from the U.S. stock market.

Life on Hold: Social Cost of Trump’s Tariffs

Economic implications and shifts within American society have been direct consequences of said agenda, causing huge uncertainty for U.S. households. A recent Harris Poll conducted for the Guardian this month revealed that six out of 10 Americans have decided to halt major life decisions and plans, including marriage, starting families by having children, buying homes and other social behaviours due to the economic anxiety and uncertainty. This is mainly due to affordability concerns and broader economic uncertainty.

Despite the administration’s efforts to boost birth rates (e.g., “$5,000 baby bonus”), most potential parents (65%) are too financially uncertain to have children. Similarly, economic instability and unaffordable housing have derailed plans for 75% of prospective home buyers. Younger generations, especially Gen Z and millennials, are disproportionately feeling the impact of rising living costs, with many reporting worsening expenses for groceries and utilities.

On a political level, where views directly shape public perception, fewer Republicans now believe the U.S. is in a recession (40% vs last year’s 67%), while most Democrats and Independents remain significantly concerned. A significant number of Independents (64%) see the economy deteriorating, a view closer to Democrats (73%) than Republicans. Skepticism also surrounds Trump’s tariff policy, with a notable portion of Americans (29%) anticipating it will negatively affect their household finances in 2025, despite the administration’s “greater America” promises.

Recession Fears and Mixed Economic Signals

U.S. recession is no longer past tense, as fears are once again growing amid Trump’s presidency and suggested policies. Anxiety rose to alarming levels at both Wall Street and Main Street, with Goldman Sachs placing odds of an expected recession at 45%. UBS outlook remains optimistic, backed by its beliefs in trade deals which would eventually avert a downturn. Other entities, including Apollo Global Management’s economist, places odds of recession at high chances closed to 90%, backed by their beliefs in the ineffective implementation of Trump’s trade strategy and economic agenda.

Negative economic indicators across various spectrums painted the picture darker, with a contraction of 0.3% in GDP during Q1 25, and unemployment climbing from 3.4% to 4.2%, technical definitions suggest that another negative quarter with the same indicators is enough to trigger a recession. Worth mentioning that according to a broader measure used by the National Bureau of Economic Research, a recession could only happen over a prolonged and widespread period.

Recession odds within Wall Street, vary widely; Morgan Stanley predicts recession odds at 40%, 60% at JPMorgan while former Treasury Secretary Larry Summers prediction exceeds 60%, along with the termination of 2 million jobs and a significant drop of $5,000+ in household income in case of a recession. On the other hand, the current administration denies at every turn recession speculation, with POTUS and top officials dismissing all economic weakness indicators, blaming it all on the previous administration and its policies.

Across the various sectors, different markets are affected, which can be drawn from their figures: gold prices surged to a record of $3,400/oz, a significant 20% reflecting caution amongst investors, while Brent Crude oil prices dropped to their lowest levels since 2021, reflecting a slower global demand amid this instability. Amid all this instability, consumer confidence decreased drastically with key indicators reflecting the sharpest drops since 1990, however resilient until this moment, with retail sales increasing 1.4% over March, contradicting/slamming negative forecasts.

While a 90-day truce on U.S.-China import duties has slightly eased U.S. recession worries, the fiscal outlook is worsening. This comes ahead of a crucial congressional vote on President Trump’s sweeping tax-cut bill and follows Moody’s recent sovereign credit rating downgrade on May 16. Consequently, on any entity level, although this step lowered recession predictions, however, it was simply insufficient to create a turnout; JPMorgan lowered their prediction to below 50%, while Goldman Sachs to 35%, still, these figures reflect the current precarious state of the U.S. economy. Any escalation particularly within the tariff situation beyond the current ones, could significantly increase trade tensions and trigger a greater economic downturn.

Indeed, amid Trump’s aggressive new tariffs cornered the U.S. economy, placing it on the verge of a critical turning point, with increasing concerns for a potential recession and risks of stagflation. Supporters of the recession-risk view cite persistent inflation, noting that the personal consumption expenditures (PCE) price index jumped to a 3.6% gain for the quarter—up sharply from 2.4% in Q4 2024. Excluding food and energy, core PCE rose to 3.5%. They also point to rising job losses, with layoffs surging by 93% in Q1 2025, attributing much of this to the economic drag from tariffs. Conversely, critics point to resilient wage growth outpacing inflation and an expanding services sector. Despite three Fed interest rate cuts last year, inflation remains high at 2.4%, worsening consumer sentiment and increasing inflation expectations to 6.5%.

This persistent inflationary pressure, exacerbated by the tariff situation, is directly reflected in consumer behaviour and outlook. The consumer sentiment index of the University of Michigan shows a significant drop in May to a preliminary reading of 50,8%, a 2.7% decrease from April’s figure “52.2%.” A vast majority of surveyed individuals expressed their uncertainty when it comes to Trump’s tariff policies, expecting them to drive inflation up significantly. The reduction in Chinese import tariffs did not achieve the expected outcome in altering the overall negative economic outlook, though creating a minimal improvement.

Rising inflation readings as well as Q1 25 contraction in GDP present cross-signals for the Fed. Despite the central bank’s consideration of lowering interest rates due to the negative growth, persistent inflation could force policymakers to hold the implementation of this course of action. Many indicators including markets pricing at June’s meeting rate cut and a total of four moves by the end of the year show that the Fed will prioritize economic growth over inflation. As consumer spending and job addition increase, the GDP report raises several flags, including recession dangers and increasing the stakes for the current president to negotiate trade deals. Further trade policy escalation, particularly tariffs, risks dragging the U.S. into a severe economic collapse causing turbulence within the global economy. Such a collapse, particularly in the current economic landscape, would be a complete disaster. The global economy is already on a precarious footing, with chronic inflation eroding purchasing power, high interest rates restricting investment, and geopolitical tensions causing widespread uncertainty.

Intertwined Destinies?

U.S. Economy’s Global Significance

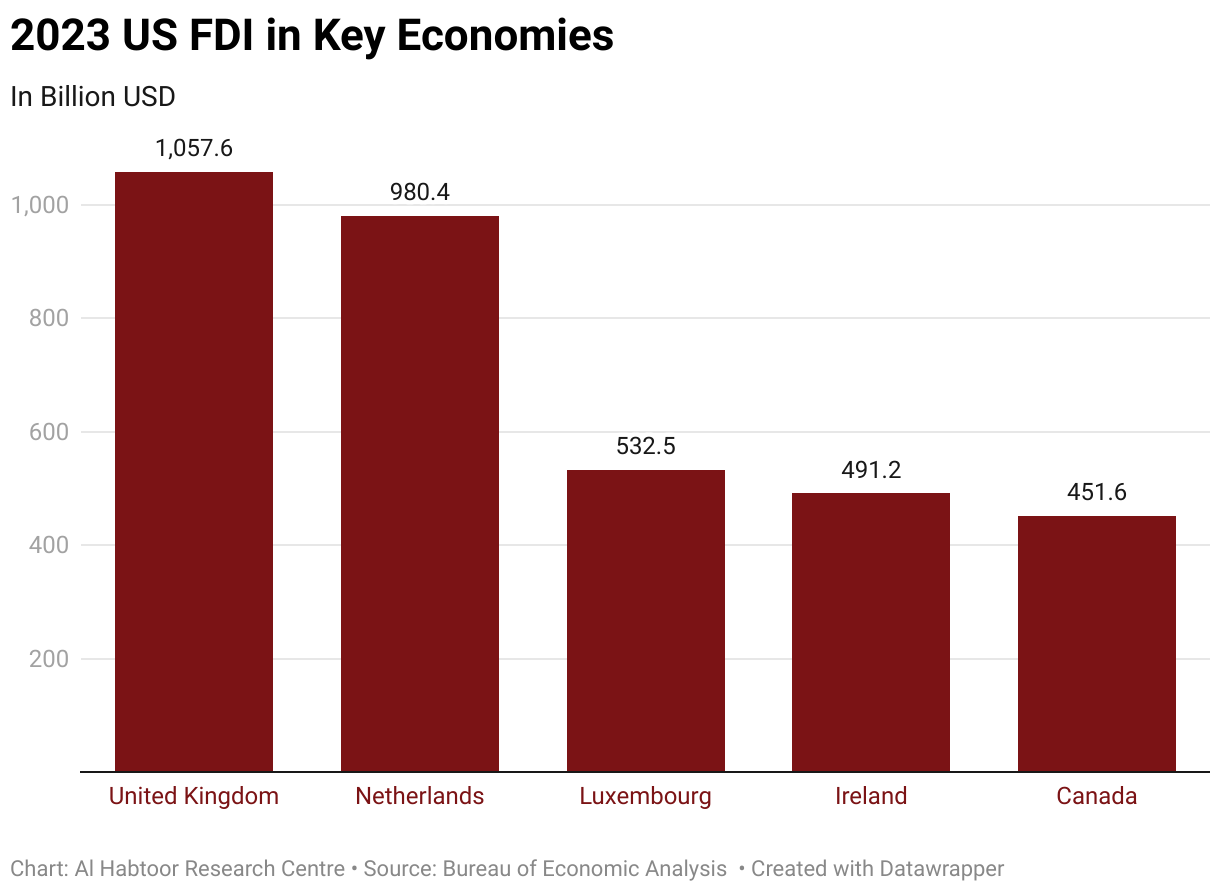

The U.S. is the largest economy in the world representing 15.56% of GDP after adjusting for purchasing power parity (PPP). The U.S. economy acts as a leading engine and one of the main fuels of any economic activity, any developments within the U.S. economy inevitably ripple across international markets with the immense consumer market, strong innovation, and sophisticated financial systems influence global growth, trade, and investment flows it enjoys. Indeed, the U.S. remains the largest recipient of foreign direct investment (FDI) globally standing at $5.4 trillion in 2023, and the leading source of outward FDI heavily investing in numerous countries worldwide, reflecting its central role in global investment flows. A shortage of this outward FDI from the U.S. can lead to a reduced FDI inflow for these recipient countries, potentially hindering their economic growth, job creation, and technological advancement.

Furthermore, the U.S. is the largest importer and the leading exporter of assorted goods and services, mainly in fintech, education, aerospace, energy, automotive, technology sectors and entertainment. Despite having a lower trade-to-GDP ratio compared to the economies of other advanced nations, the substantial size of the U.S. domestic market indicates that its trade volume dominates a notable portion of global trade flows, estimated at one-tenth of global trade. Hence, any changes within the country’s economic policies would have substantial impacts and effects on various international players, including trade partners, strategic allies, and supply chains.

Beyond Borders: Key Sectors in Peril

The U.S. economy is vastly interconnected, thus placing economic stability at the top of the priority list to any ruling regime. Any collapse within the economy of such a major player would only harm significantly global trade. Time and again, the U.S.’s recent tariffs and trade wars have proven their ability to disrupt global supply chains and reduce GDP worldwide in a collapse scenario. Reducing demand for goods and services from the U.S. would eventually affect exports from other countries, as export-driven economies “China, Germany, Mexico, and Canada among others” rely heavily on U.S. consumption.

If the U.S. economy collapses, U.S. imports will drastically cause factory closures and massive layoffs, while heavy manufacturing regions will suffer from a deteriorating GDP. This profound impact extends beyond general economic downturns, directly threatening key global sectors such as automotive, electronics, and machinery, dependent on integrated global supply chains, would be especially hard-hit, as both demand and financing dry up.

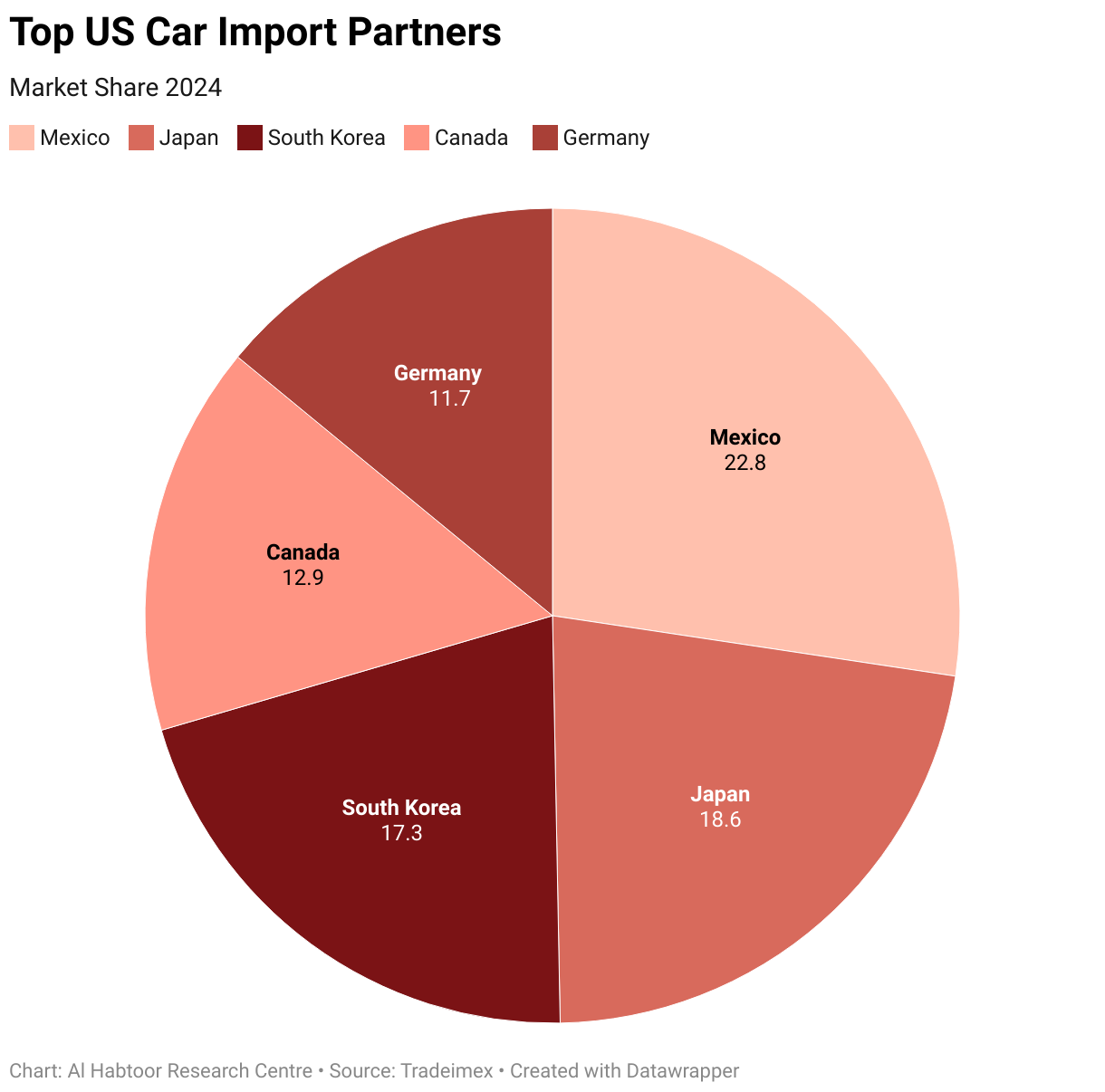

Automotive Industry: The collapse of the U.S. economy, a major importer of vehicles and spare parts, especially from Mexico, Canada, Japan, and Germany would mean a demand reduction, impacting production lines and exports across these nations. This is particularly true for Canada, Mexico, and the EU, whose automotive exports collectively form a significant portion of the U.S. market. Shipping lanes and trade routes within both the United States-Mexico-Canada Agreement (USMCA) region and the trans-Pacific/trans-Atlantic region would suffer from a decline in automotive cargo.

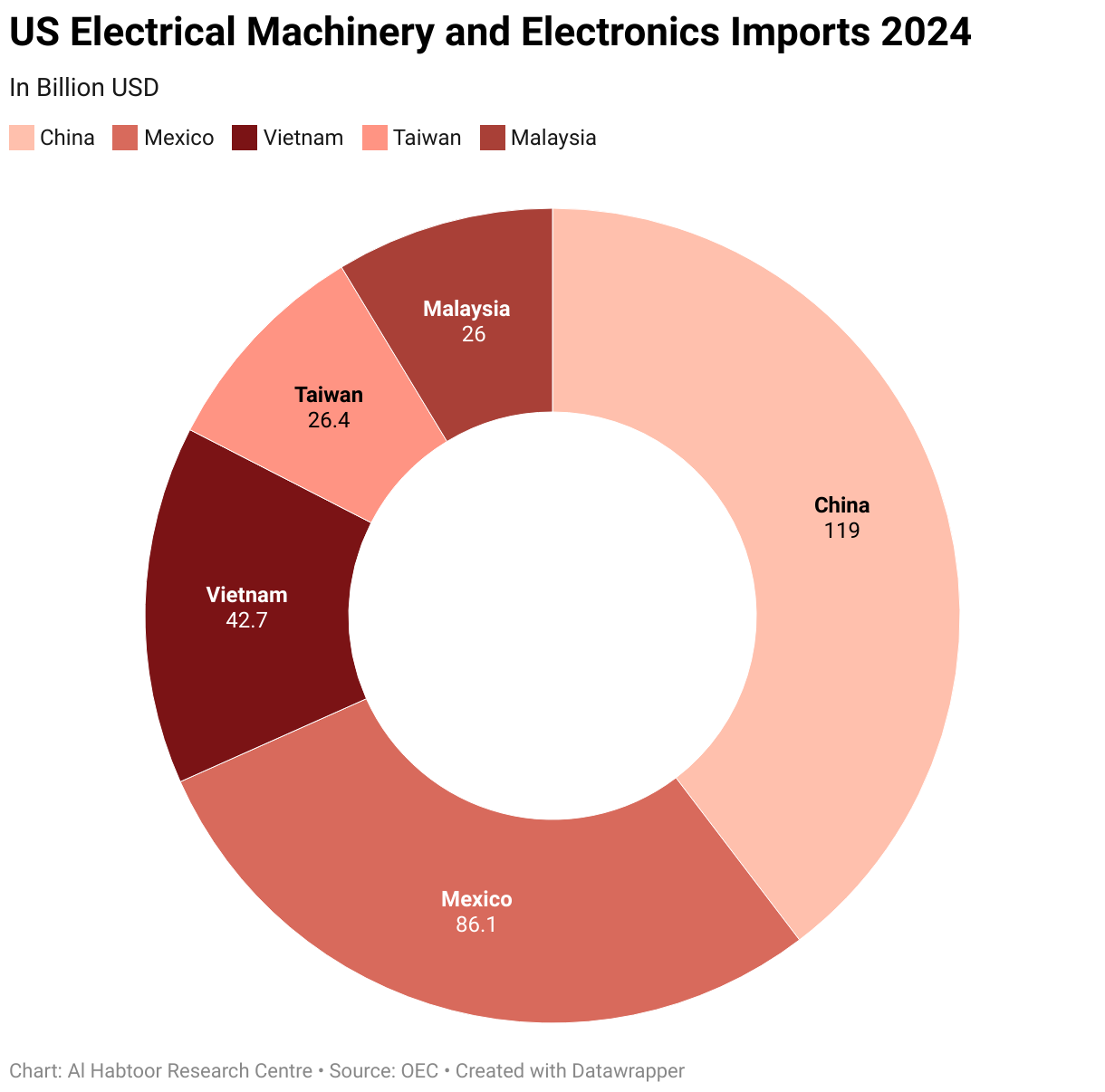

Electronics: In addition to the automotive industry, the U.S. is a major consumer and importer of electronics, with top beneficiaries including China, Taiwan, South Korea, and Vietnam. A decline in U.S. demand would severely affect these nations, leading to a reduced number of shipments across the Pacific. For instance, South Korean tech manufacturers would suffer from a drop in their sales figures, as the U.S. heavily rely on their smartphones and electronic appliances. Similarly, countries like China, Vietnam, Bangladesh are key exporters of apparel and textiles to the U.S. A U.S. economic downturn would lead to decreased demand for these goods impacting shipping routes across both the Indian Ocean and the Pacific.

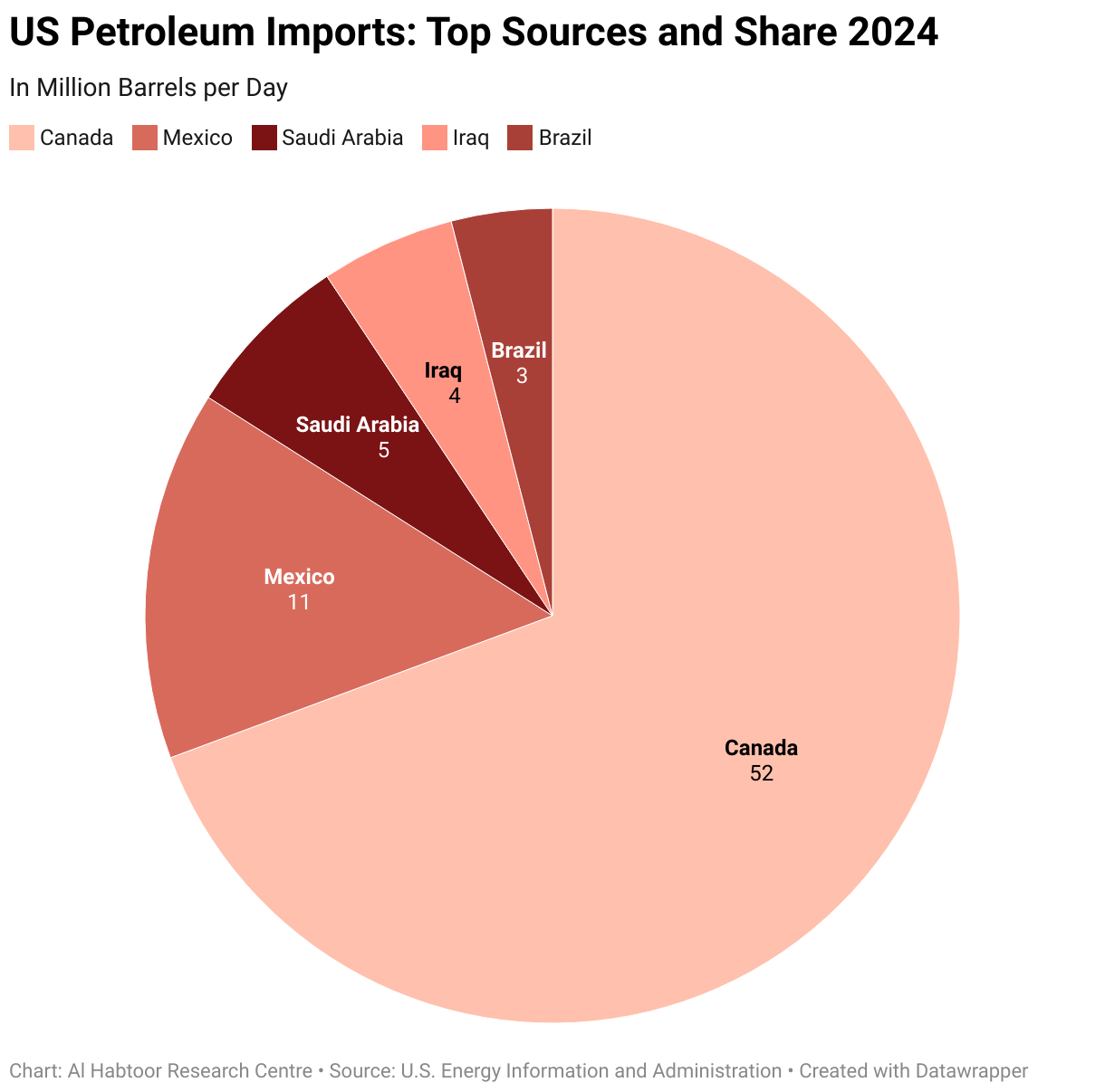

Energy and Commodities: A sudden decline in U.S. industrial and consumer activity would lead to a drop in global oil and gas demand, pushing prices to decline sharply, affecting energy markets across the globe. Countries like Saudi Arabia, Russia, and Nigeria among others that rely heavily on petroleum revenues for national budgets will be severely affected.

On an equal level, a sharp decline in industrial metals and agricultural commodities demand will mostly harm manufacturers in Latin America, Africa, and Australia.

Tourism: Rapid contractions would affect the tourism sector worldwide, as the U.S. is considered one of the major players in outbound tourism. The declining number of tourists would affect countries and regions that rely on tourism revenues from U.S. visitors, including regions in the Caribbean, Southeast Asia, and parts of Europe that saw the highest number of U.S. tourists in 2024. Tourism-related industries including airline companies, hotel chains, and luxury retail outlets worldwide would suffer significant declines in revenues.

Agriculture: Being both a major importer and exporter of agricultural products, a collapse in the U.S. economy would disrupt trade flows. For instance, the U.S. imports fruits, vegetables, and other food products from Mexico, Canada, and South America, hence, a decline in demand and consumer spending would decrease the mentioned countries’ exports to the U.S., impacting land transportation across the USMCA border and shipping routes from South America.

Real Estate: The U.S. investment flows, which considerably benefits international real estate markets in major countries could see their market suffer from net capital outflow and price declines. Production pace in construction-related sectors such as steel, cement, and equipment manufacturing would also slow down, due to reduced infrastructure and property development activities bound with U.S. demand.

Financial System and Currency Impacts

A possible collapse in the U.S. economy, apart from the immediate impact it will have on reducing the country’s demand, could also trigger an unprecedented wave of protectionist measures, as many countries will attempt to protect their local industries and economies from any global fallout which in turn, will further suppress global commerce. Additionally, such a collapse could create devastating consequences affecting the global financial system, given the fact that the U.S. is the world’s largest economy and the largest issuer of primary reserve currency (USD).

Worldwide stock markets would likely plunge, due to a global state of panic among investors amid a sudden disappearance of U.S.-based cash liquidity, most of whom would rush and allocate investments in alternative instruments including gold, other currencies and potential digital assets. Currency wars and tensions would rise across borders, as devaluation would remain one of the few options to be implemented by different central banks globally to stay in the game. Banks that are directly exposed to U.S. assets or their clients, particularly in Europe, Japan, and emerging markets could get exposed to liquidity shortages. Several countries in emerging markets around the world could face sovereign debt crises, as they hold significant amounts of USD denominated debt, given the U.S. defaults on its obligations or in the event of the volatility of the USD. The USD dominance over international trade and finance calls for a potential devaluation following a U.S. collapse, as it will lose its value drastically, creating complex consequences and shifting the balance of economic power. Other suffering countries would be the ones pegged to the USD, as they will face imported inflation, capital flight, and increased pressure on their foreign exchange reserves to maintain the peg. Moreover, a forced devaluation strategy could backfire, and destroy investors’ confidence and driving up borrowing costs for the U.S. While a weaker USD might theoretically boost U.S. exports, the overall economic turmoil would likely negate such benefits. Furthermore, a collapse of the U.S. economy would destabilize the foundation of global finance, incapacitating institutions like the IMF and rendering their mechanisms ineffective in a worldwide financial crisis.

The alarming possibility of a U.S. recession, as reflected in recent warnings from financial institutions across the world such as the IMF, acts as a reminder that even any small-scale economic disturbance or decline can cause significant economic effects across various economies. Subsequently, a U.S. economic collapse can initiate a financial disaster of unprecedented magnitude across borders. In a more-than-ever-before interconnected world, any collapse will ultimately harm every nation, painting a new horizon for the international political and economic landscape for decades to come, as other countries would inevitably step in to fill the vacuum left by the U.S. in their global economic and political roles.

This analysis is part of the “What If” series, available on AHRC website under the Early Warning Program.

References

CNN Business. “Consumer Sentiment Falls in May: Preliminary Data.” CNN, May 16, 2025. https://edition.cnn.com/2025/05/16/economy/consumer-sentiment-may-preliminary

Forbes. Saul, Derek. “Recession Odds: GDP, Economy, Labor Market, Unemployment, Consumer Confidence.” Forbes, May 6, 2025. https://www.forbes.com/sites/dereksaul/2025/05/06/recession-odds-gdp-economy-labor-market-unemployment-consumer-confidence/

Global Business Alliance. “Foreign Direct Investment in the United States: 2024 Report.” Global Business Alliance, 2024. https://globalbusiness.org/foreign-direct-investment-in-the-united-states-2024/#TopInvestors

International Monetary Fund (IMF). World Economic Outlook, April 2025: Navigating Policy Trade-Offs. Washington, D.C.: IMF, April 22, 2025. https://www.imf.org/en/Publications/WEO/Issues/2025/04/22/world-economic-outlook-april-2025

International Monetary Fund (IMF). “Foreign Direct Investment Increased to a Record $4.1 Trillion.” IMF Blog, February 20, 2025. https://www.imf.org/en/Blogs/Articles/2025/02/20/foreign-direct-investment-increased-to-a-record-41-trillion

J.P. Morgan. “Recession Probability.” J.P. Morgan Insights. Accessed May 18, 2025. https://www.jpmorgan.com/insights/global-research/economy/recession-probability

Nomad. “The Most Popular Travel Destinations by US State in 2024.” GetNomad Blog, 2024. https://www.getnomad.app/blog/most-popular-travel-destinations-by-us-states-2024

Reuters. “Goldman Sachs Cuts US Recession Odds to 35% from 45% on Trade Truce Optimism.” Reuters, May 13, 2025. https://www.reuters.com/markets/us/goldman-sachs-cuts-us-recession-odds-35-45-trade-truce-optimism-2025-05-13/

Reuters. “Weak US Economic Outlook Persists Despite Brief Trade Truce with China.” Reuters, May 21, 2025. https://www.reuters.com/world/china/weak-us-economic-outlook-persists-despite-brief-trade-truce-with-china-2025-05-21/

Statista. “United States: Share of Global Gross Domestic Product (GDP) from 2018 to 2028.” Statista, 2025. https://www.statista.com/statistics/270267/united-states-share-of-global-gross-domestic-product-gdp/

The Guardian. “Americans Worry About the Economy as Trump Gains in Polls.” The Guardian, May 12, 2025. https://www.theguardian.com/business/2025/may/12/americans-economy-trump-poll

TheStreet. “Goldman Sachs Unveils Tariffs Prediction, Recession Forecast.” TheStreet. Accessed May 17, 2025. http://thestreet.com/economy/goldman-sachs-unveils-tariffs-prediction-recession-forecast

United Nations Conference on Trade and Development (UNCTAD). “Trade Tensions and Rising Uncertainty Drag Global Economy Towards Recession.” UNCTAD, 2025. https://unctad.org/news/trade-tensions-and-rising-uncertainty-drag-global-economy-towards-recession

World Trade Organization (WTO). Trade Outlook 2025. Geneva: WTO, 2025. https://www.wto.org/english/res_e/publications_e/trade_outlook25_e.htm

Related Articles

What If: The Turkish Judiciary Invalidates the 2023 CHP Leadership Elections?

What If: The Middle East Burns Next?

What If: As-Suwayda Sought Independence?

What If: The UN Runs Out of Money?

What If: Iran Attacked the Dimona Reactor?

What If: Iran Closed the Strait of Hormuz?

What If: China Invades Taiwan?

What If: The India-Pakistan Ceasefire Collapses?

What If: Israel Created a New Corridor to the Euphrates in Syria?

The Ozempic Shockwave: How Is One Drug Impacting Global Food and Insurance Systems?

What Would Iran’s Withdrawal from the Nuclear Non-Proliferation Treaty Mean?

The Semiconductor Cold War: U.S. vs. Russia, China and India

Domino Effect: Are More States Moving Toward Recognising Palestine?

From Isolationism to Intervention: Trump’s MENA U-Turn

Sports Diplomacy and the Reduction of Global Political Tensions

Crossroads: The Battle for the Soul of the Democratic Party

Iran and Israel: The War That Will Redraw the Middle East

Red Alert: Potential US Attack on Iran

Why Did Iran Fail to Repel Operation Rising Lion?

Why the Houthis Insist on Attacking Israel?

Comments